The IPO Lawsuit Trap Is Real. The Quiet Period Isn’t the Trap.

I went looking for nuisance lawsuits during the SEC quiet period. The data pointed to a broader public-company litigation tax.

At the end of every board of directors meeting we always went into executive session. Those were my favorite part of board meetings. The formal meeting had a pre-read, motions, approvals, committee reports, and all the other machinery that makes corporate governance work. Executive session was different. A handful of smart people got to sit around and talk about what they were actually worried about.

One of those conversations once revolved around a simple question: what if we want to IPO someday?

One of the arguments against it was the ubiquitous perception that once a company filed for an IPO it would have to deal with nuisance lawsuits during the quiet period. My definition of a nuisance lawsuit is a baseless lawsuit aiming for a settlement that costs less than the lawyers’ billable hours to get it dismissed. More colloquially, it is a shakedown.

During parts of an IPO, the company is inside an SEC-regulated quiet period. It cannot freely talk in public. So if someone files a contrived lawsuit during that window, the company cannot defend its reputation the way a normal private company might. It has lawyers, bankers, auditors, SEC comments, investor roadshow preparation, employee questions, board pressure, and a ticking clock. The extortion logic is obvious: file something embarrassing, make it cheap enough to settle, and dare the company to risk the IPO timeline over principle.

I obviously feel pretty strongly here. I have dealt with my share of attempted shakedown nuisance lawsuits, and never gave in to the attempted bullies.

One of the things I have been doing on sabbatical is researching the “I wonder” thoughts that pop into my head. With all the chatter about possible SpaceX, OpenAI, and Anthropic IPOs, this one came back. I wanted to test the startup community’s folk wisdom: do companies get swamped by shakedown lawsuits while they are trying to go public and cannot defend themselves?

So I pulled public data and built the study.

The question: what do the SEC, federal dockets, Delaware courts, and IPO filings show about lawsuits during the IPO run-up compared with the before-S-1 and after-IPO periods?

The answer is annoying in the way useful answers often are.

I was right about the general direction. Going public really does attract lawsuits.

I was wrong about the clean version of the mechanism. The SEC quiet period is not where the data says the generalized shakedown spike lives.

Those are my favorite experiments.

Results up front

This is long, and I do not expect most people to read the whole thing. The rest of the post tells you how I got here. The headline result is this:

The quiet-period shakedown hypothesis, as a population-level claim, does not hold up. Companies in the SEC quiet period are sued a little more often than in the 180 days before filing the S-1, but not enough for me to trust it as a separate phenomenon. The confidence intervals overlap. The shakedown-like score is not higher in the quiet period. If anything, the quiet period looks less shakedown-heavy than the before-S-1 and mature public-company windows.

But the broader intuition is real. Companies going public attract much more litigation than companies staying private.

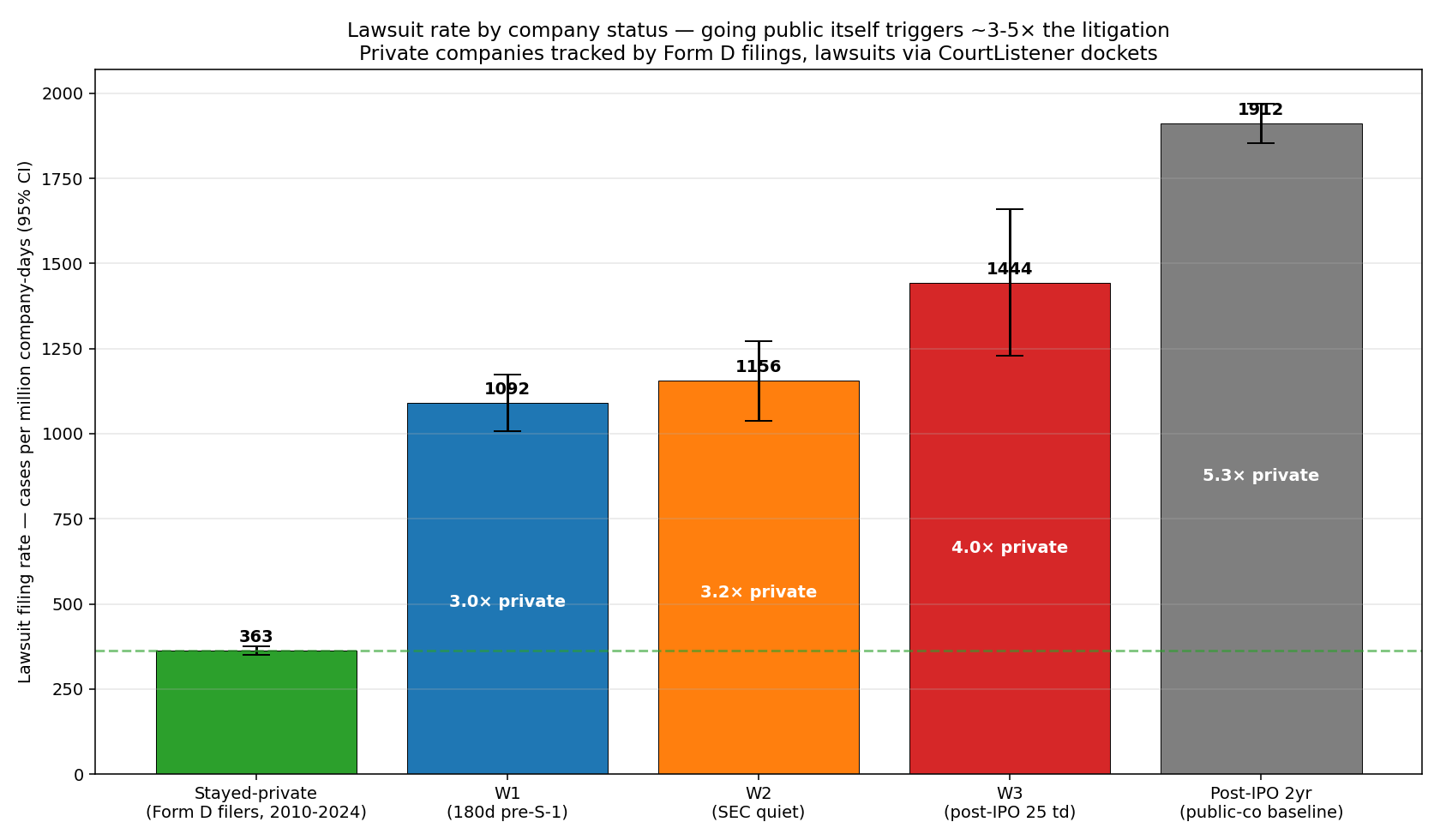

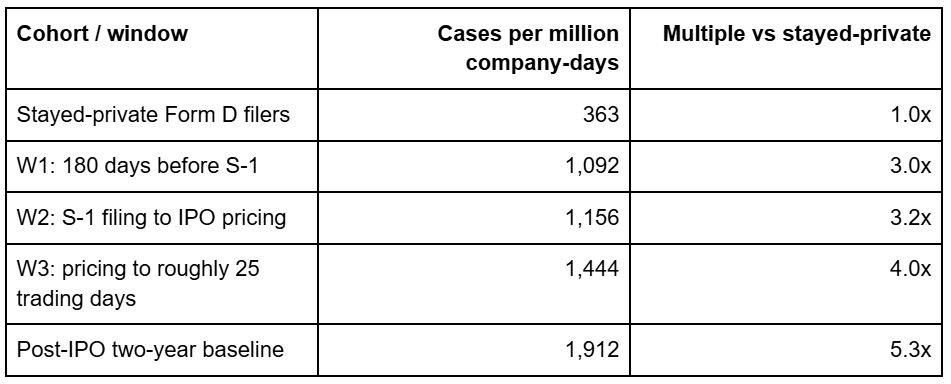

The rate for stayed-private Form D companies was 363 federal cases per million company-days. IPO companies were already at 1,092 per million company-days in the 180 days before filing the S-1. They were at 1,156 during the quiet period. They were at 1,444 in the first roughly 25 trading days after pricing. In the two years after the IPO, they were at 1,912.

That is the big reframing. Becoming a public-company-in-progress appears to carry a roughly 3x litigation premium before the S-1 is even filed, and a roughly 5x premium after the company is public.

So if your question is, “Should I be afraid that filing an S-1 creates a unique quiet-period shakedown window?” my answer is mostly no.

If your question is, “Does going public move the company into a different litigation environment?” my answer is yes. Very much yes.

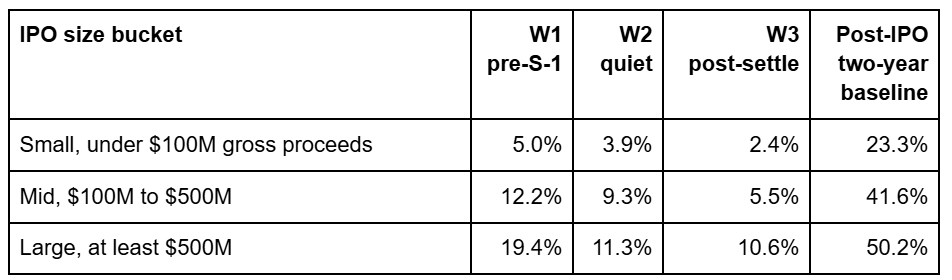

The core table

The specific quiet-period step from W1 to W2 is only about 6%. W1’s 95% confidence interval was 1,009 to 1,175. W2’s was 1,039 to 1,272. Those overlap. I would not build a board-level theory on that difference.

The public-company transition, however, is not subtle.

What I measured

I built the IPO universe from SEC EDGAR filings, not from a commercial IPO database. The heuristic was deliberately mechanical: a company needed the S-1 or F-1 registration statement, the 424B final prospectus, and the 8-A exchange registration sequence that marks a real public listing. SPACs and blank-check companies were filtered out.

Final universe: 3,399 non-SPAC U.S. operating-company IPOs priced from January 1, 2010 through May 26, 2026.

Then I matched those companies against two federal lawsuit corpora:

27.6 million CourtListener federal civil dockets through March 31, 2026.

4.58 million Federal Judicial Center Integrated Database cases, which have richer plaintiff, defendant, disposition, class-action, and procedural fields, but effectively end around 2021.

The FJC data is better for understanding case outcomes. CourtListener is better for modern coverage. So the study uses both.

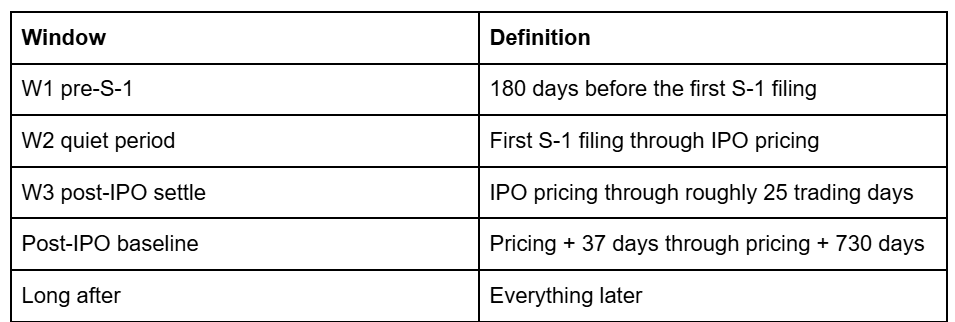

I split each IPO timeline into the windows that matter legally:

The name matching is always the part of this kind of study where the bad data tries to kill you. Corporate names are messy. Subsidiary names are messy. Former names are messy. “Hudson” is a company name, a person name, and an invitation to false positives.

So I used strict name normalization and fuzzy matching, then LLM verification to estimate false positives. That matters because a naive docket match overstates the litigation rate. A lot of cases that look like company matches are not the same corporate entity.

The article numbers use the verified true-positive estimates where available. The exact decimals are less important than the shape:

stayed private -> pre-S-1 -> quiet period -> post-pricing -> public-company baseline.

The line goes up.

But the quiet-period step is not the story.

Finding 1: the quiet-period spike mostly is not there

The thing I expected to see was a lawsuit pileup inside W2, the S-1-to-pricing quiet period. That is the window where a company is preparing for the roadshow, working through SEC comments, and trying very hard not to create a new disclosure problem.

If nuisance lawyers were timing lawsuits to maximize leverage, this is where I expected them to show up.

They did not show up at the population level.

W1 was 1,092 true-positive cases per million company-days. W2 was 1,156. That is directionally higher, but barely. W3 was 1,444, and the post-IPO two-year baseline was 1,912.

The Facebook-style post-pricing stock-drop burst is real. The mature public-company lawsuit environment is real. The quiet-period shakedown wave, as a generalized IPO deterrent, is not.

That does not mean no shakedowns happen during the quiet period. They do. I found them. Yes, they still made me mad.

It means the founders’ common wisdom is overfit to the most emotionally salient cases. If a founder hears about a startup being sued five days before pricing, that story lodges in the brain. It lodged in mine. But the rate data says that story is not the dominant structure.

Finding 2: going public is the litigation event

The private-company baseline changed how I read the whole project.

I sampled 5,000 stayed-private companies from the set of issuers that filed multiple Form D notices but never filed an S-1. The observation window was first Form D through last Form D plus 730 days, capped at March 31, 2026. Then I matched those companies against CourtListener dockets the same way.

The stayed-private rate was 363 federal civil cases per million company-days.

By the time a company is in the six months before its S-1, the rate is about 3x that. That is before the public filing. Before the quiet period. Before CNBC knows what to say about the ticker.

Some of this is selection. IPO companies are larger, richer, more visible, more likely to have national operations, and more likely to be in regulated markets than the average Form D filer. A perfect test would compare IPO companies to size-matched, industry-matched, late-stage private companies. That probably requires PitchBook, Crunchbase, or another commercial data source.

But selection does not make the result unimportant. If you are a founder, C-suite, board member, or investor, you do not care whether the lawsuit premium is metaphysically caused by the S-1 or by the company becoming big enough to file one. You care that the company is entering a litigation environment with a different base rate.

That is the thing to plan for.

Not “quiet period equals lawsuit ambush.”

“Public-company transition equals lawsuit magnet.” I would hire a general counsel ahead of an IPO.

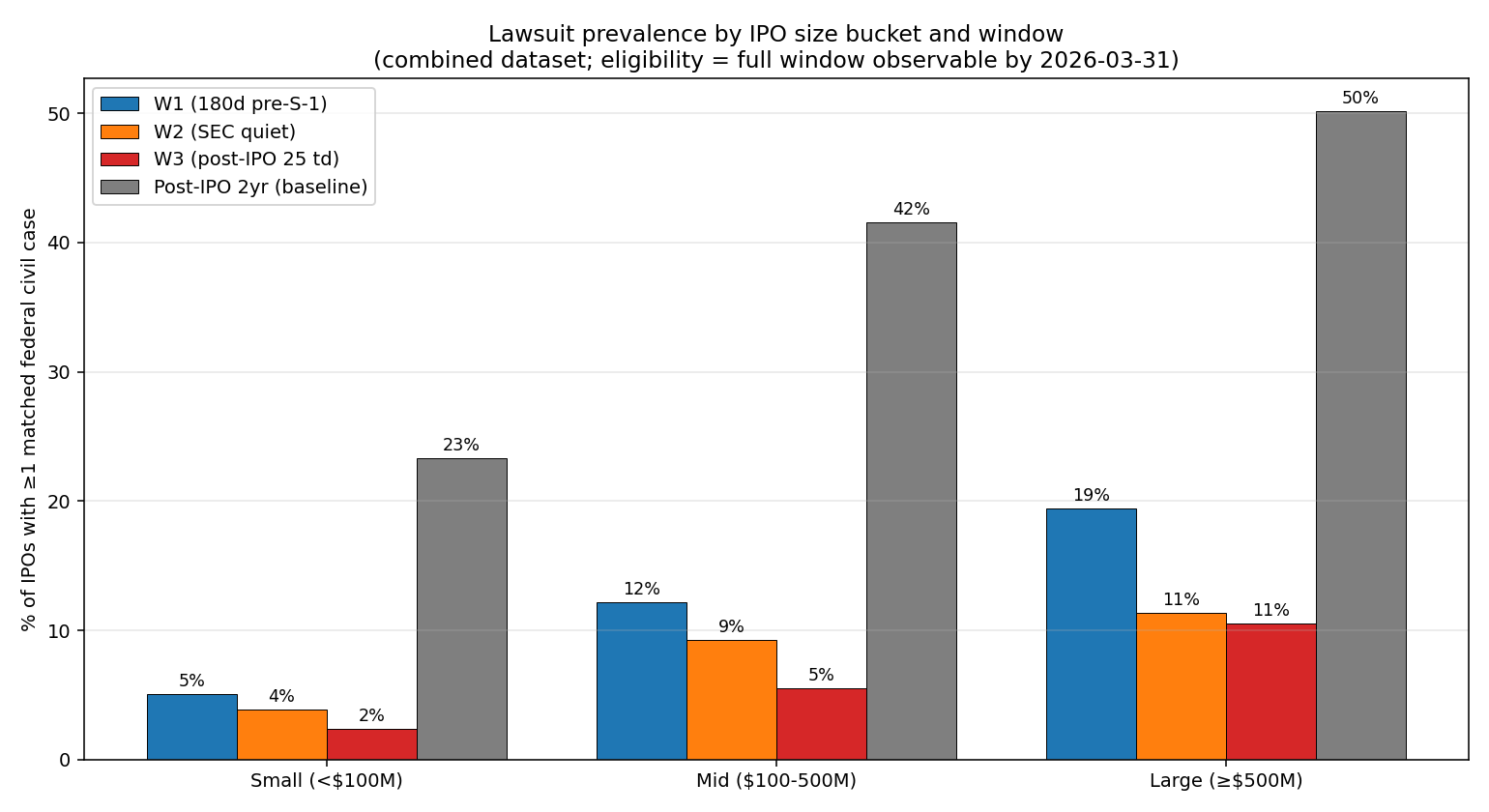

Finding 3: company size matters

Lawsuits scale with company size. That is not surprising, but the slope is useful.

Large IPOs face about 3x the quiet-period lawsuit prevalence of small IPOs. But again, the quiet-period column is not the most dramatic column. The post-IPO two-year baseline is.

By the time a large company has been public for two years, half of them have at least one matched federal civil case.

This is where I think a lot of private-company boards misunderstand the tradeoff. They talk about IPO litigation as if it is a special ambush during the transaction. The transaction matters, but the bigger change is that the company becomes visible, liquid, analyst-covered, plaintiffs-firm-searchable, and governed by a very different disclosure regime.

You did not just ring a bell. You changed the company’s surface area.

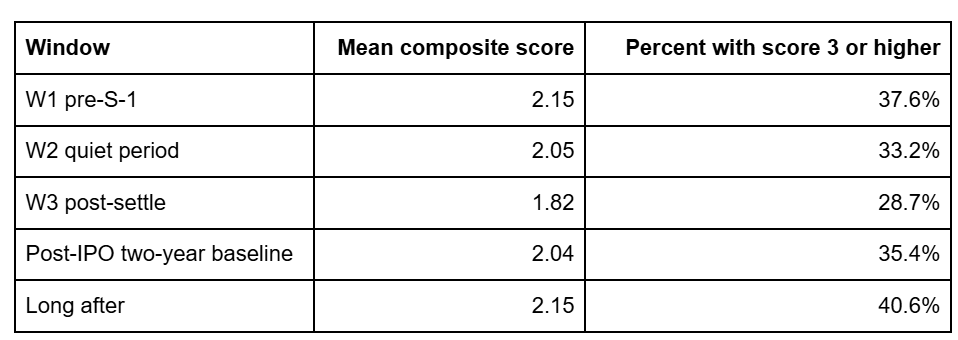

Finding 4: quiet-period cases are not especially shakedown-like

I built a shakedown composite score because “that feels like a shakedown” is not a methodology.

The score is crude but took my emotion out of it. It gives one point for each objective signal:

Fast resolution.

Dismissal-like or low-value resolution.

Repeat plaintiff.

Minimal docket activity.

Solo individual plaintiff.

No-press signal, which is currently a placeholder because I did not need to integrate a news database for the patterns to jump out.

Composite score ranges from 0 to 6. I treated 3 or higher as shakedown-like.

On the FJC-scored subset, the quiet period did not stand out:

This is the part that most directly cut against my prior. If the quiet period were uniquely attractive to nuisance plaintiffs, W2 should have had a visibly higher shakedown-like share. It did not.

But the aggregate hides some interesting pockets.

The W2 quiet-period cases that looked most shakedown-like were not primarily securities cases. They were small personal-injury claims and Fair Labor Standards Act wage-and-hour cases. I had the model review 48 W2 cases in those buckets. Ten looked shakedown-like. None were textbook mobster-movie shakedowns, but some were exactly the kind of narrow, badly timed lawsuit a company might pay to make disappear.

Examples:

Airbnb had a personal-injury claim filed 7 days before IPO pricing.

US Foods had an individual personal-injury case resolved in 22 days.

HD Supply had an individual FLSA case filed shortly after the S-1 and ended through motion judgment dismissal.

Ignite Restaurant Group had a personal-injury claim filed on the IPO pricing date and resolved in roughly two months.

That is real. If you are the GC or CFO inside that transaction, you do not get to dismiss it as “not statistically significant.” You have to deal with it while everything else is on fire.

But at the market level it is a small cluster, not the structural reason companies stay private.

Finding 5: there are trolls under the bridge

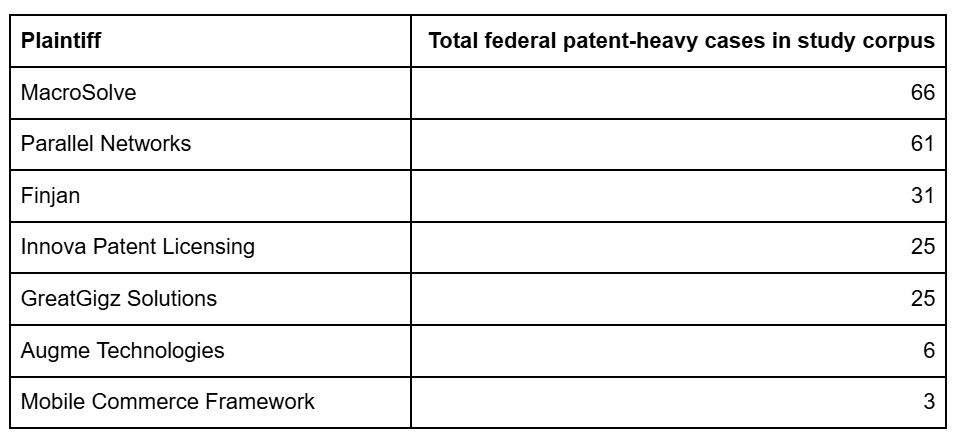

I expected the repeat-law-firm map to be messy. It was not. The top repeat plaintiffs targeting multiple IPO issuers around the run-up windows were overwhelmingly patent assertion entities.

Those seven plaintiffs filed 217 total federal cases between 2009 and 2021 in the study corpus, overwhelmingly patent cases.

This is the most industry-like pattern I found. It is not mass litigation against every IPO company. No repeat plaintiff was carpet-bombing the IPO universe. But the character of the data is consistent with patent assertion entities understanding that a company in the IPO pipeline has a different settlement calculus.

The twist is that patent cases during the quiet period did not score as especially shakedown-like under my simple composite. That may be because the composite is better at detecting low-effort nuisance suits than patent monetization campaigns. A patent case can be a shakedown and still require a real docket, much higher priced lawyers, and enough procedural substance to avoid looking like a one-page demand letter with a case number. Or maybe the IPO filing is what brought an infringement to the patent owners’ attention. I’ve never been on either side of a patent fight so I don’t have a good gauge if these were nuisance or legitimate.

Consent judgment matters here. A consent judgment is not evidence that a case was serious. It is often exactly what a successful settlement looks like: both sides agree to end the fight, the defendant removes uncertainty, and nobody has to find out how much or little substance the patent had.

The better signal is speed. Across the LLM-flagged non-disclosed cases, about 43 resolved in under 90 days. That is the zone where the “pay them to go away before the IPO” theory becomes plausible.

So yes, patent assertion entities are part of the story. They are just not the whole story.

Finding 6: the S-1 disclosure story is noisy, not scandalous

I also wanted to know whether companies were hiding these lawsuits from IPO investors.

For the 323 IPOs with a matched pre-IPO federal civil case in W1 or W2:

69.0% disclosed pending litigation in the S-1 legal proceedings section.

7.1% had only boilerplate “from time to time” language.

23.8% had no specific litigation language.

That sounds bad until you compare it against IPOs without a matched pre-IPO case:

66.3% disclosed pending litigation.

6.3% had boilerplate only.

27.3% had no specific litigation language.

In other words, the S-1 legal-proceedings language is noisy. Lots of companies disclose litigation risk generically or disclose ordinary-course matters. The presence of a matched federal pre-IPO case did not create a giant visible disclosure gap.

So I did a deeper review of the 100 non-disclosing IPOs with W1/W2 matched federal cases. Two different LLMs judged the same case-company pairs for entity match and whether the case should have been disclosed. The aggressive OpenAI pass flagged more than my local Nemotron (and I was already out of Claude API tokens today). The more defensible cross-LLM consensus set was 66 cases across 39 distinct IPOs.

That is 1.1% of the 3,399 non-SPAC IPO universe.

Names in the consensus set included Alibaba, General Motors, DoorDash, FireEye, Hilton, Twilio, Palo Alto Networks, Peloton, Robinhood, Chegg, Berry Plastics, Acacia Communications, Berkeley Lights, ContextLogic, Coursera, Freshworks, JELD-WEN, Natera, SendGrid, SmileDirectClub, and loanDepot.

That is not zero. It is not even uninteresting. Some of those should make securities lawyers sweat.

But it is not a giant hidden population of companies secretly shaken down in silence before going public.

A realistic broader estimate is probably 60 to 100 IPOs out of 3,399 with some combination of non-disclosed pre-IPO litigation and nuisance-settlement signatures. Call it roughly 2% to 3% on the high side. The clean consensus number is closer to 1%.

Small in absolute terms. Painful if you are in the unlucky set.

Finding 7: Delaware Chancery was a dead end

One theory was that federal dockets were missing the real action because pre-IPO shakedowns might be hiding in Delaware Chancery.

I probed Delaware Court Connect for the 100 non-discloser IPOs across the S-1 minus one year to pricing plus one year window.

There were 273 Delaware hits:

That makes sense after thinking about it for ten seconds longer than I initially did. Chancery fiduciary-duty litigation generally requires shareholders. Before the IPO, the future public shareholders do not exist yet. After the IPO, Chancery becomes relevant. Before the IPO, not so much.

California Superior remains the state-court gap I most want to close, especially for ADA tester and California employment cases, but they hide their cases behind a captcha that makes this type of mass study tricky. Regardless, Delaware Chancery is not where the missing quiet-period shakedown wave is hiding.

What I got wrong

My mental model was too transaction-centered.

I thought the quiet period itself was the vulnerability: the company cannot talk, so plaintiffs time lawsuits for maximum reputation pressure.

That mechanism exists. I still believe it exists. I found examples consistent with it.

But the data says it is not the dominant structure. The dominant structure is visibility, scale, liquidity, and becoming searchable in the machinery of public-company litigation.

The nuisance lawsuit risk does not start when the SEC quiet period starts. It starts before the S-1, when the company is already large enough, visible enough, and rumor-visible enough to be an IPO candidate. It grows after pricing, because now the company has public shareholders, daily stock movement, analysts, short sellers, plaintiffs’ firms watching the chart, and a much larger disclosure target.

That is the thing I did not understand before.

The boardroom folk wisdom was directionally right and mechanistically wrong.

That distinction matters. If you solve for the wrong mechanism, you build the wrong defenses.

What this means for founders and boards

Do not stay private because you are afraid of a generalized quiet-period lawsuit ambush. The data does not support that as a market-level reason.

Do treat the IPO process as the start of a new litigation regime.

The practical work starts earlier than most companies want it to. I could give you a list of all of the things you should do to pre-emptively mitigate nuisance lawsuit risk. But you’re paying your investment bankers and external counsel a small fortune and this is one of the areas they really earn their keep.

I now understand, viscerally, why public companies hire internal General Counsel. Not “a lawyer.” Not “outside counsel can handle it.” A real internal owner whose job is to understand the company’s risk surface, the disclosure regime, and that capitulating to a bully once will lead to more bullies.

The private-company instinct is often to treat legal as a cost center. The public-company reality is that legal becomes part of the operating system.

The answer

Is the common wisdom wise or foolish?

Both, which is the most annoying answer and usually the correct one.

Foolish version: “The SEC quiet period creates a wave of nuisance lawsuits that is a major reason companies stay private.” The data does not support the litigation wave, even if founders believe it.

Wise version: “Going public changes the litigation environment, and companies should expect more fights.” That is strongly supported.

The difference between a stayed-private company and a post-IPO public company is about 5.3 times as many federal civil lawsuits per company-day in this dataset. Even before the S-1 is filed, IPO-bound companies are already at about 3 times the stayed-private rate.

Someone once gave me a signed Babylon 5 (Science Fiction TV show) photo, and I added one of the show’s quotes to it: “Never start a fight, but always finish one.”

I still believe that when dealing with shakedowns.

I also understand the public-company version better now. Going public does not just create one big transaction. It creates a company that has to finish many more fights. Some are real. Some are nonsense. Some are timing weapons. Some are the predictable cost of being large, visible, liquid, and worth suing.

As someone who never gave in to a threatened shakedown lawsuit, that is a lot of fights to finish.

And now I understand why the General Counsel has an office next to the CFO.