The Founder's Guide to M&A: Lessons from Selling a Defense Tech Company

Preamble

Kudu Dynamics was founded in 2013 as an offensive cybersecurity defense contractor. Many people helped us along the way, and several previous founders explicitly told us they were “paying it forward” from those who helped them. This guide continues that tradition, arming technical founders, C-suite leaders, and board members with hard-won insights from the M&A process.

What follows presents the M&A timeline from both perspectives: the company being acquired and the acquirer. Each step highlights potential landmines and exposes unsavory M&A behaviors to help you navigate the process successfully.

Mike Frantzen

Founded Kudu Dynamics in 2012 as a solo founder without external investors, but with the ambitious goal of building an offensive cybersecurity organization designed to truly scale. As a technical founder, he competed in DEF CON Capture the Flag, discovered zero-days, built capabilities, and operated on target. After 12 years as CEO and $400M in R&D revenue, he learned the business side through blood, sweat, and tears; experiences many readers will have shared.

Adam Sheipe

Still Mike writing… For you CEOs out there, you’ll find that people are often reluctant to brag about themselves, so you have to do it for them. Early in our process I talked to numerous Investment Bankers and Corporate Development executives. I’ll explain that more later. Almost everyone I talked to I asked “who else should I really be talking to in order to understand how the M&A game is played.” Adam is one of the few people that almost everyone mentioned as both a master of the M&A game, and as a nice guy. He’s probably blushing right now. He agreed to help write this, to bring the Buyer’s and M&A expert perspective to this guide, and gleefully to help quash the chicanery we saw from some unsavory buyers.

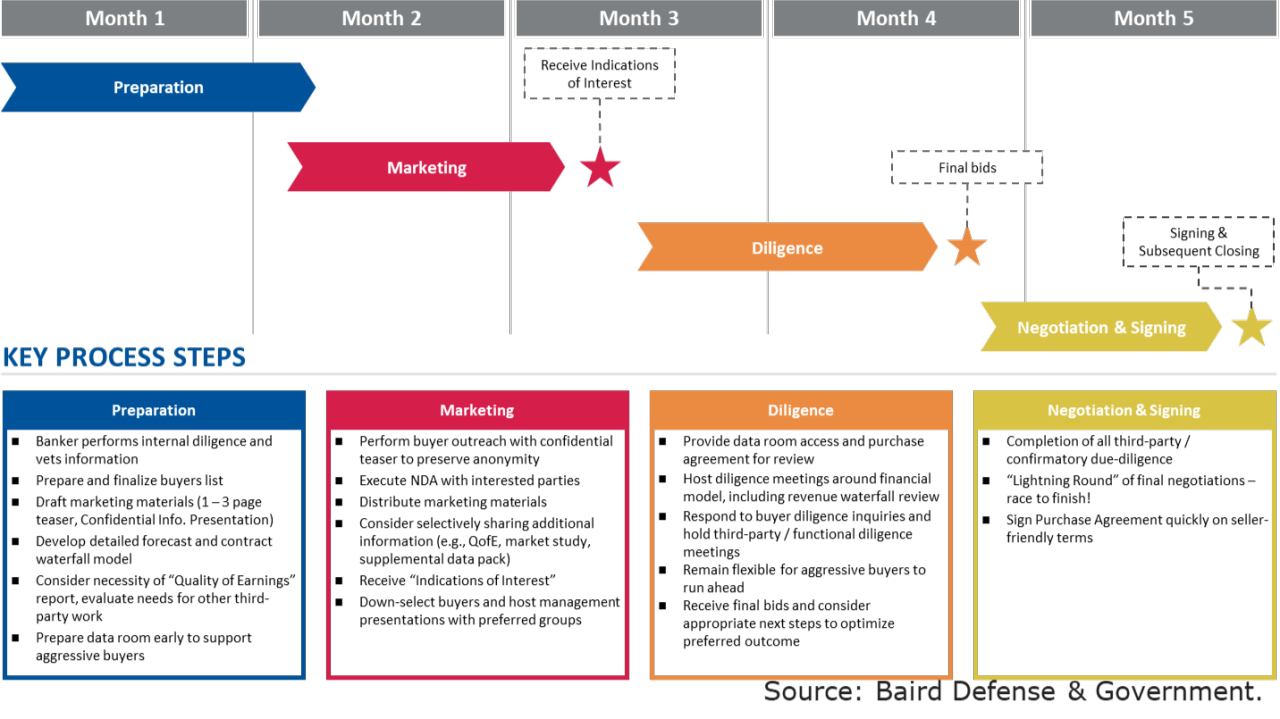

The Seller’s M&A Timeline

Step -1: Before You’re For Sale

The Universal Truth: You are always for sale. If you have shareholders or a board, you have a fiduciary duty to consider unsolicited offers. Even as a sole shareholder, there’s probably an offer, monetary or otherwise, you wouldn’t refuse. Once you cross $1M in EBITDA, you’re on someone’s acquisition target list.

Building Relationships with Investment Bankers

Investment bankers are worth their weight in gold (literally, I checked the spot price). Their business is selling businesses, so they know your market’s value drivers better than you might. They’ll share insights because they want to eventually sell your business and earn their commission. Meanwhile, prospective buyers regularly consult with these bankers; you want to be top of mind when a strategic buyer needs exactly what you offer.

Specific Recommendation: Identify all investment bankers who have bought or sold your competitors. Meet with them annually to:

Assess market conditions

Review your business fundamentals

Understand what commands premiums vs. discounts

Position yourself for unexpected opportunities

Specific Recommendation: Factor what you learn from the bankers in to how you operate the business.

Note: The market dynamics described below are from our experience and have likely changed. This volatility is another reason to maintain regular banker relationships.

Key Market Intelligence to Gather

EBITDA Thresholds, Multiples, and the changing Buyer Universe

In our market, specific EBITDA levels commanded higher multiples: $1M, $3M, and $10M

At lower levels, say under $5m, large buyers may decline to spend time citing the adage, “is the juice worth the squeeze”. At this level the buyer universe may be limited to financial sponsors executing a roll-up of multiple small companies.

In the mid-range, say high-single digits to $50m, larger buyers come into play, along with financial sponsors who are looking for a “platform” on which to build a rapidly growing business (organically and inorganically).

Above $50m the set of strategic buyers who can deploy the capital required to close a deal starts to shrink quickly. Larger private equity firms will remain in play looking at the business as a platform for future growth. At this stage, you have become a “big bet” for any buyer.

Above $100m, the buyer universe shrinks to a handful of large strategic and private equity players. An IPO may be in play (though be sure to fully assess the hazards of being public before considering that route!)

Your banker can advise as to your buyer universe which you should at least contemplate during your regular teaming discussions as you grow and operate the business.

Contract Type Considerations

Small Business set-aside contracts vs. full and open competition (many buyers assume set-asides evaporate upon acquisition and will exclude them from their assessment of your value).

SETA contracts and potential conflicts of interest which may constrain your buyer universe.

Sub vs. Prime contracts (larger strategic buyers may assume that any work you have as a sub to their competitors will evaporate upon acquisition and will exclude that work from their assessment of your value unless you can demonstrate that the prime simply can’t perform without your contribution)

Contract types: CPFF vs. Award Fee vs. T&M vs. FFP vs. OTA vs. SBIR (and within SBIR, Phase I and II vs. III)

ODCs vs. Labor revenue (and within labor revenue, direct labor vs. sub labor) vs. Product sales

Product Resale vs. Native IP driven Product vs. Services revenue

Operational Factors

IT systems integration (mature buyers know this can make or break an acquisition)

Proposal win rates (we deliberately wrote some proposals for training, accepting lower win rates)

Documentation and process maturity

Fringe benefit compatibility (we were an ESOP and needed a really solid answer to “what happens if it goes away?”)

Compliance and management processes maturity

Early Preparation Activities

Several initiatives we implemented for business growth directly contributed to M&A value:

Leadership Depth and Breadth We built a deep bench to sustain high growth. Buyers valued this for both upside (foundation for continued growth) and downside protection (resilience if key people left). This also provided capacity to maintain business growth during due diligence. For anyone who will make “boat money” in a deal, you should have depth chart / succession story to tell.

Audited Financials Three years of externally audited financials (required by our bank) caught mistakes early, allowing corrections before they became M&A issues. Cost: ~$50K/year with a regional firm.

CRM Discipline We documented all business development opportunities in a CRM (Customer Relationship Management), which became critical for our M&A waterfall discussions. It is also important to have a documented logically defined procedure/policy for assigning probabilities (go and win) to your pipeline opportunities (and never put 100% on anything that isn’t signed and sealed… that will erode credibility, especially if 100% goes to 0% during your process!)

Written Policies and Procedures Comprehensive documentation helped during due diligence. Warning: We lacked IP Assignment agreements in our onboarding which could have killed the deal. Ask your counsel for a buy-side due diligence list for corporate hygiene matters. Looking at yourself through the lens buyers will apply in their risk assessment will (a) help you patch gaps, and (b) prepare you for questions to come.

Skeleton Management Every rapidly growing organization accumulates organizational debt. Address it continuously. Due diligence will find most issues, so pay down organizational debt before going to market. This should be a regular activity for you, every quarter or at least every year. Avoid “spring cleaning” right before your go to market and having to tell your profit story through quality of earnings adjustments.

The Go-to-Market Decision

The board and leadership team must decide whether to pursue a sale or respond to unsolicited offers. Here’s the hard truth: You will regret either choice. Choose “yes” and regret the change. Choose “no” and regret missing the opportunities M&A brings. Accept this paradox.

Our Approach: Each board member defined their litmus test for what shareholders would likely accept which included factors beyond just financial metrics. For our ESOP, the Trustee developed criteria reflecting employee interests. We then consulted bankers to project likely outcomes. When assessments exceeded our litmus tests, we went to market. And we went to market right before an unsolicited offer came in.

Left of Launch: Building Your Deal Team

Selecting an Investment Banker

Your Investment Banker (called banker but don’t confuse them with your local deposit bank) quarterbacks the entire process. They understand your market, competitors, and buyers often better than you do. They wield soft power, potentially restricting future deal flow to buyers who behave badly.

Ask your bankers what to expect from each buyer you allow into your process. While there are universal truths about categories of buyer and how they think about driving value, your banker should be able to tell you how each individual buyer will act in the process… who is fast, who is slow, who bids high and then works the price down, and who you can trust to do what they tell you they will do. Your banker should also explain each buyer’s decision-making process… how do they make decisions, who are the decision makers and who can you trust at the buyer to accurately communicate what the ultimate decision maker is likely to do.

Remember that it is your business. You are the client. You want to pick a banker who will fight to achieve your goal, your aspiration, and give you honest feedback when your goal or aspiration may overreach the likely outcome. You want to avoid at all costs any banker who suggests the deal or process is theirs… they are a facilitator; you own the outcome.

Our Selection Process:

Identified bankers from competitors’ M&A press releases

Held preliminary meetings under NDA

Reviewed their pitches and proposed buyer lists

Key Innovation: Asked bankers to introduce us to their proposed buyers’ Corporate Development (Corp Dev) leads

Interviewed these Corp Dev executives about each banker’s strengths and weaknesses

Made our selection based on buyer feedback

Key Insight: by interviewing those Corp Dev executives you are communicating that you will be on the market shortly so they will have their people, advisors, and budget pre-approved.

Caution on Operational Security: Bankers who leak competitor information during pitches will leak your information too. We chose a Banker who protected competitor information. While this risk exists regardless because you are going to divulge your proprietary information to many of your competitors as potential buyers, run your process quickly to minimize exposure.

We chose Baird. They are awesome.

Legal Counsel and QoE Providers

Ask your chosen banker for their recommended counsel and Quality of Earnings (QoE) firms. They’ll suggest partners who excel and collaborate well. Interview their recommendations and choose teammates you’d want in the foxhole at 2 AM on four hours of sleep. Let me footstomp the importance of great legal counsel. They will be there at 2 AM for every crisis and often will be working through the night so it’s handled before you meet with buyers that morning. It will happen a lot.

Pro Tip: Have your counsel negotiate your contract with the banker for you. They understand market terms and can level the information playing field.

Pro Tip 2: Similar to bankers, you want to pick counsel who will fight for your desired outcome. Avoid at all costs counsel who wants to test the latest art of transaction structure or deal terms on your deal. Let others who don’t know better pay for the privilege of being the test case.

Life Pro Tip: Cheap lawyers are far more expensive than expensive great lawyers.

We chose Cooley LLP as Counsel and Pipaya Partners, LLC for QoE. They are awesome.

Building Your Internal Deal Team (Pre-Launch)

You’ll need key employees across multiple functions to support due diligence: Business Development, IT, Finance, HR, Security, Contracts, and potentially Facilities. This team will make or break your deal execution.

Selection Criteria:

Choose people who can maintain absolute confidentiality

Select those who can handle extreme workload without dropping their day job

Favor those with attention to detail and spreadsheet skills

Consider personality fit since they will be on camera with buyers at 6 AM and 11 PM

Build redundancy and expect to use it

Be cautious selecting anyone who might hold the process hostage at crucial moments. Some employees, recognizing their temporary leverage during diligence, have been known to demand extraordinary compensation or threaten to withhold cooperation. We’ve heard horror stories.

Transaction Bonuses: It’s customary (and essential) to offer transaction bonuses to compensate for working regular jobs plus nights and weekends on the deal. These bonuses:

Ask your banker for market rates and to understand what buyers will accept

Pay out only after successful close (aligns incentives)

Should be documented in writing before heavy lifting begins

May include accelerated vesting or retention components

Tactical Execution:

Phased Involvement: Don’t burn out your team early. Bring in:

Finance and BD first (for waterfall and QoE)

HR and IT during initial due diligence

Security and Contracts for specialized sessions

Facilities only as needed

Information Compartmentalization: Not everyone needs to know everything:

Limit valuation knowledge to essential personnel

Triple check everyones’ calendars are private. Whoops

Don’t bring people in too early, or too late

Workload Management:

Block calendars proactively for deal work

Set up dedicated communications channel

Keep the business performing because buyers are watching metrics

Critical Warning: Your most senior people will be pulled into the deal. Ensure deputies step up to maintain operations. A declining business during due diligence will either kill the deal or reduce price.

Documentation Tip: Create a shared tracker showing who’s handling which diligence requests. Buyers often ask the same question multiple ways looking for inconsistencies.

Waterfall Development (~2 Months to Launch)

The waterfall is your current and projected revenue weighted by probability. According to Baird, it is “the battleground of M&A” and they were right (as usual). Buyers will build models determining maximum purchase price based on your waterfall. They will ask for explanations of every entry multiple times over several meetings. Inconsistencies directly reduce their estimated probability of win (pwin) which directly reduces valuation.

Critical Requirements:

Use a CRM to track every opportunity

Define and document your pwin methodology such that you follow it and can share it.

Record detailed opportunity notes (customer interactions, timelines, dependencies)

Include low-probability opportunities that buyers might improve post-acquisition (but be honest in your assessment of what you can do on your own to maintain credibility)

Prepare to explain every entry multiple times to every buyer

Prepare to explain every entry multiple times to every buyer

Be truthful. Buyers will know or have trusted consultants on the calls who know the customers.

Example of Good Documentation: “On [date], we encountered the customer in the hallway. They confirmed the RFP timeline but mentioned parental leave starting [date], potentially delaying release by three months.” This communicates deep customer understanding, ability to walk the halls (which could have huge value to a buyer if they don’t have that access), and an accurate pwin.

Quality of Earnings (~1 Month to Launch)

QoE firms calculate your EBITDA with “add-backs” and defend it to buyers’ auditors. At a 15x multiple, every dollar added back to EBITDA means $15 in purchase price. This becomes a battle of reputations where buyers typically use Big 4 firms. Trust your bankers when picking a QoE firm.

Understanding Add-Backs:

Good add-backs: Expenses that disappear post-acquisition (external board compensation, stock valuation costs)

Problematic add-backs: Large owner draws/dividends implies founders will leave or accept lower compensation after acquisition which might not be true. Also be wary of add-backs that may erode credibility (e.g. we added back $X of expense last year because we have a new vendor who could have done the work for less).

Work with bankers to optimize add-back strategy years before going to market. Credibility is everything in your add-backs (though your banker will correctly advise you to be on the aggressive end of credibility!)

Pre-Due Diligence (~2 Months to Launch)

Before going to market, expect your banker to run you through preliminary due diligence. This critical step identifies and fixes skeletons in your closet before buyers find them.

What to Expect: In the final auction, each buyer will ask between 300 and 3,000 questions. For example:

Buyer 1: “Break down workforce demographics by veteran status, PhDs, masters, and bachelors degrees”

Buyer 2: “Identify PhD count by experience: >20 years, 10-20, 5-10, and <5. Same for masters and bachelors”

Notice these are similar questions requiring different data cuts. Different parts of the same buyer or different representatives of the same buyer may ask overlapping questions (your banker should help you manage this with the buyer if it becomes a common occurrence… most buyers do not intend to be redundant, but some are more organized than others). Due diligence will be exhausting.

Key Actions:

Fix identified issues now! Delays now are better than deal-breaking surprises later

Upload all source materials to a datasite

Let banker associates answer what they can from documentation

Remember: “We have that data from the last 2 months” beats “We don’t track that”

Why This Matters: Buyers (and you) don’t want surprise liabilities from a stock sale. You don’t want them reducing the price to insure for liabilities that don’t exist. Clean it up now.

Articulate Your “Why” (~1 Month to Launch)

Every buyer will ask why you’re selling and why now. They’ll be skeptical of your answer and desperately trying to understand who on the leadership team will stay, under what conditions, and for how long. Private Equity will likely insist on significant equity rollover to ensure key people remain. They may be buying your leadership team.

Do Your Soul Searching: What do you all want?

Strategic Positioning: Work with your banker to align your go-to-market strategy with these desires:

If some leaders want to retire, have those planning to stay take center stage

Leaders who want to continue should articulate their goals clearly such as: specific areas they need help in, less people management, more resources, acquisition opportunities, and for PE: A “second bite at the apple” (cash out now, 4x the remainder later).

Our Approach: We chose brutal honesty about our objectives, probably to our bankers’ chagrin. We footstomped three objectives at the beginning and end of the CIP and in every management presentation: what we needed help with to accomplish great things (which would also make money).

This clarity revealed which potential acquirers:

Aligned with our objectives

Didn’t care as long as they made money. This isn’t bad, they will probably give you total freedom as long as you make your numbers.

Were not savvy enough about our market to understand either

The CIP: Your Company’s Story (~1 Month to Launch)

The Confidential Information Presentation is a comprehensive slide deck covering all business aspects. Key insights:

Fundamental Truth: You are not your programs or people. You are:

A process for winning and executing programs

A process for recruiting, training, and retaining talent

A system that scales

Your intellectual property

Present programs and people as proof points of your processes’ effectiveness. Identify where buyer resources could accelerate your scaling. And understand it’s ok to overrule your bankers where you know your market better than they.

On Classified Work: You cannot hide behind “it’s classified.” Review your Security Classification Guides and determine what’s unclassified. Buyers have heard “it’s classified” from companies with nothing behind the curtain. Give them something concrete to justify your price to potentially uncleared boards. Where you are constrained by classified content, find a way to tell the story about the solution you provide or value you add by analogy, without disclosing classified content. Your buyers will appreciate the effort you make here, and it is an opportunity to add a bit of creativity/fun to the overall presentation.

Information Security Reality: Your entire CIP will go to competitors who may keep it for reference despite NDAs. Choose between protecting secrets and maximizing value. We chose full transparency knowing they couldn’t recreate our systems anyway and Adam Sheipe thinks we were smart enough to recognize that buyers would not pay us for value we did not tell them about.

Preparing a List of Potential Buyers (~1 Week to Launch)

Your banker will present a list of companies they think might be interested and some that they know are looking to buy someone like you to fill a strategic gap. This is your opportunity to remove companies from the list or even add some where you know the landscape better.

Expect Surprises: We talked to all potential buyers and were frequently surprised:

Several companies we thought would have no interest were actually very eager to enter our domain via acquisition

Several we expected to trigger bidding wars weren’t even interested (reasons: existing acquisitions in progress, still integrating previous deals, couldn’t swing the financials)

Critical Lesson: Strike companies you have deep intrinsic problems with early but after you give them a chance. One particularly unethical company went out of their way to throw sand in everyone else’s gears to attempt to poison the process. Removing bad actors early:

Conserves your resources for genuine fits

Saves good-faith buyers from wasting money before they spend millions in due diligence

Sends a message about acceptable behavior

Puts you on a path to end up with a buyer who you want to work with

Be careful about carrying preconceived emotions, positive or negative, about any buyer into the to the process. The fact that one of your key executives had a bad experience with someone from the buyer in the past may come down to a single actor at the buyer and have very little to do with how you should evaluate the buyer generally. Similar with a good experience.

In Hindsight: We should have removed bad actors as soon as they showed their colors, rather than letting them poison the process.

Understanding Buyer Types in Defense/Government Services

In our industry, buyers fall into three distinct categories, each with different motivations, deal structures, and post-close implications for your team:

1. Strategic Buyers (Highest Valuations, Least Autonomy)

Who They Are: Large companies (usually public, some family-owned) seeking specific capabilities or market access.

What They Bring:

Mature infrastructure (systems, processes, past performance, etc.)

Established customer relationships and contract vehicles

Deep pockets for investment

Immediate scale advantages

Valuation Dynamics:

Pay highest premiums when you fill a strategic gap

Value synergies they can’t replicate organically

Will model revenue acceleration using their resources (why you’re worth more)

Will put a value decrement on risk, even if the risk is just perceived/hypothetical

Deal Structure:

Usually all-cash or cash plus buyer stock

Sometimes earnouts for aggressive growth projections (be cautious, earnouts are often suggested as a creative way to bridge a valuation gap, but rarely work the way the parties intend)

Post-Close Reality:

Your brand will eventually disappear

Expect system migrations to aggressively scale

Less autonomy but maximum resources (to aggressively scale)

Your people will have increased opportunities across the breadth of the buyer’s business, but may eventually pine for the entrepreneurial spirit that helped your company get to where it is

PowerPoint… forests of PowerPoint

Best For: Founders seeking maximum value or the maximum injection of new resources and who don’t mind loss of more identity/control. Founders who place significant value on more growth opportunities for their people than a small business can offer.

2. Platform Creation (PE Creating New Consolidator)

Who They Are: Private equity firms buying a company in a sector to build upon.

N.B.: There may not be any PE firms looking to build a new platform in your sector. See Platform Bolt-Ons

What They Bring:

Capital for aggressive acquisition strategy

Experienced operating partners

Professional board governance (and a requirement for control by the private equity owner)

Clear exit timeline (3-5 years)

Valuation Dynamics:

Pay market rates and sometimes a significant premium when they have a track record of successful platforms in the sector

Focus on EBITDA quality and growth potential

Value management team highly

Look for bolt-on acquisition runway

Deal Structure:

Significant rollover required (20-50% of proceeds)

Management incentive pool (percent of equity)

Critical: They’ll likely bring in their own CEO and/or CFO

Your leadership team shifts to senior leadership below their CEO

Post-Close Reality:

You become the acquirer of smaller companies

Rapid pace of bolt-on acquisitions (could be 3-5 per year)

Focus shifts to integration and synergy capture

Second bite potential: 3-5x rollover in good scenarios. Many people expect to make more from the rollover than the initial sale… but your returns will be subordinate to the minimum returns of the private equity firm.

Best For: Leaders who want to build something bigger and can accept new leadership above them; or want to take cash out with another large bite at the apple.

3. Platform Bolt-On (Fastest Close, Tolerant of Skeletons in your Closet)

Who They Are: PE-backed platforms executing their consolidation strategy.

What They Bring:

Established integration playbook with synergy targets

Some centralized services

Valuation Dynamics:

Lower multiples unless highly strategic

Heavy focus on cost synergies

Customer overlap affects price

Deal Structure:

Mostly cash with modest rollover (10-30%)

Shorter diligence and negotiation

Post-Close Reality:

Back-office consolidated quickly (finance, HR, IT)

Your culture, plan, and career subordinated to platform leadership’s

Your senior leadership may end up part of the synergy story

You better like the word synergy

Best For: Founders seeking quick exit with less complexity but accepting lower valuations but potentially a quicker second bite at the apple.

Launch Day

Follow your banker’s system precisely. Expect:

Phone calls from the bankers to the buyers

Teasers sent out

NDA negotiations

CIP distribution

Initial buyer conversations

This might be your only break and it could last just one day. Rest while you can.

When Deals Leak (Throughout Process)

Assume Everything Will Leak. Our deal leaked that we’d sold to private equity before we were even on the market and it was a customer’s SETA contractor feeding the rumor mill. Plan for leaks from day one, because they’re inevitable.

Stakeholder Response Strategies

Employees:

Develop a consistent response consistent with your culture before going to market. And expect to use it without any advance warning.

Our approach: Lean into rumors with humor: “I heard we sold to Private Equity three months ago, do you know who my new boss is?”

Customers (especially government):

Emphasize continuity of service and personnel

Be prepared for customer calls

Competitors:

They’ll use uncertainty to poach employees and customers

Prepare to handle retention conversations

Document any unethical competitor behavior for future Founder’s Guides

Practical Tactics:

Code names in all communications (even verbal). Our internal name was “Red 8” as something boring and innocuous

Keep your internal read-in list tight. If people do not need to know, they shouldn’t know

Separate email threads for deal discussions. Consider using external IT

Hold sensitive meetings off-site (pick non-descript places where your buyers, competitors and other bankers do not normally congregate… e,g, not the Tysons Corner Ritz Calton!)

Vary the cover story for why executives are unavailable.

Brief your receptionist on handling unexpected visitors (and ask your guests to avoid company branded shirts, notepads, ID tags, pants, etc.)

Do your best to avoid a material untruthful cover story; you will still need the trust of your team when this is done

The Silver Lining: Sometimes leaks help because they can create urgency with buyers, and signal to other potential bidders your desirability.

Indications of Interest (IOIs) and Down Selecting (~3 Weeks Post-Launch)

Buyers submit initial price ranges and initial terms. Remember:

Successful/predictable processes drive prices up from IOI ranges; surprises can have an outsized negative impact

All terms are negotiable but pay close attention to what terms may be on their “must-have list”

Your bankers can make a phone call to see how negotiable terms/prices are

Keep only genuine contenders to respect everyone’s resources

If you need to keep a contender in only to drive up the price then understand that they are a genuine contender because you value price more than fit.

Red Flags:

If someone says “I thought you were going to punch that guy” after a meeting, you should drop them. We did

Buyers complaining about others’ “unethical behavior” while behaving unethically. Remove them, talk to your banker about restricting their future deal flow, and write a Founder’s Guide to M&A.

Buyers who avoid talking about how they see the combined business operating post-closing. It’s fine if this isn’t fully baked, but if they won’t talk about it, they either haven’t given it thought (red flag) or don’t want to tell you about what they think may not be good for you and your people (red flag x2)

Buyers who do not ask “what questions do you have for us?” or who fail to give you a presentation on who they are why they are interested in you.

Buyers who do not propose using Representation & Warranty insurance as their recourse for breaches. This is table stakes in the current 2025 market. If you do not get this you may be looking over your shoulder for years after closing.

Management Meetings (Continuous)

Two types of meetings will dominate your life:

Senior Leadership Meetings:

Present your CIP to buyer (competitor) executives

Treat these as two-way conversations

Ask about their secret sauce. They’re courting you too and will tell you.

Poor answers reveal leadership weaknesses

Rude behavior at this stage is a black flag… run away

Due Diligence Sessions:

Waterfall reviews (multiple deep dives)

Classified conversations can go into the SCIF

Functional area sessions: IT, HR, Finance, Security, Facilities, Tax

Divide and conquer with your leadership team

Demonstrating leadership team depth sends a powerful message

Poise during this stage is critical. You will have multiple buyers coming at you with multiple subject matters experts each. You will see a mix of senior and junior people and a mix of people who have a clear understanding of what each party is trying to accomplish, and people who were dropped into a meeting with no context. Treat everyone with respect and rigorously demand the same in return.

Purchase Agreement Negotiation (~2 Months)

The Share Purchase Agreement (SPA) defines all terms and closing conditions. Critical points:

Once signed, you lose all leverage

Understand every closing condition and every hook that the buyer has into you between signing and closing, and post-closing

Use your information advantage to negotiate achievable conditions

Ensure everything important is in writing before signing

There is no such thing as “don’t worry, this is just a legal issue”. If you have a question about a provision in the purchase agreement then ask your lawyers. Don’t accept the provision until you understand it.

Terms can be as important as price. Peace of mind for you and your family post-closing is priceless.

Retention and Rollover Equity (Negotiation Phase)

Each buyer’s bid will handle retention differently, and this often becomes a major negotiation point. Understanding the structures and implications is critical for successful deal execution.

Key Retention Components:

1. Retention Pool Structure

Funding: Critical distinction: does it come from purchase price (reduces seller proceeds) or additional buyer funding?

Distribution: You’ll negotiate who gets what, but buyers have strong opinions

Vesting: Usually 1-3 years

2. Employee Categories and Requirements Buyers will segment your employees into distinct buckets:

Critical/Must-Retain: Essential for value preservation (typically 5-10 people)

Golden handcuffs: 2-3 year commitments with significant retention bonuses

Often becomes a closing condition so be certain they’ll accept not only the concept, but the key terms (retention bonus agreements often include handcuffs, including non-competition, non-solicitation and non-disparagement).

Transition: Needed through integration (3-12 months)

Stay bonuses paid at specific milestones

They’re critical to integrate the two companies together

Think carefully about how you communicate this type category to the affected employees as it may become quickly apparent that some buyers do not intend to retain them long-term.

Key to Growth Opportunities: Sign non-competes/non-solicits but free to leave

Typically 12-24 month restrictions

May include garden leave provisions

Everyone: we had multiple buyers propose giving RSUs to everyone. We did. I’m still not sure if it helped more than it hurt.

3. The “Handcuff” Negotiations You’ll have multiple awkward conversations about:

Who the buyer insists must stay (their list)

Who you believe is critical (your list)

What “retention” actually means (duration, compensation, terms)

What happens if someone refuses (deal killer vs. price adjustment)

Warning: Buyers often underestimate who’s actually critical. They focus on senior titles but miss the principal engineer who actually runs everything or the BD person with all the customer relationships. The conversations are awkward but not hard – the buyer wants to get this right. You can help the buyer get to the right answer by having good logic behind each individual on your list… avoid appearing like your list is a “friends and family” list.

Private Equity Rollover Requirements:

PE buyers typically require key personnel to “roll over” equity into the new venture meaning they must reinvest proceeds from the sale back into the company in a tax-advantaged way. This serves multiple purposes:

Typical Terms:

Mandatory Minimums: Significant portion of the after-tax proceeds for C-suite

Investment Opportunity: Positioned as “second bite of the apple” with potential 3-5x returns

Retention Mechanism: Makes it expensive to leave (forfeiture provisions)

Alignment Tool: Ensures management has skin in the game

Rollover Negotiation Points:

Who Must Roll: Usually C-suite and key revenue generators (closing condition)

Who May Roll: Extended to broader leadership team (opportunity not obligation)

Minimums and Maximums: Depending on role

Terms: Same class of equity as PE firm or subordinated? Voting rights? Board seat?

Liquidity: Can they sell in secondary offerings or only at exit?

Critical Actions:

1 Pre-Deal Preparation:

Survey key employees confidentially about retention appetite

Understand who has retirement plans

Document who’s actually critical vs. who has impressive titles

Prepare for surprises–everyone is exhausted at this point

2 During Negotiations:

Push for buyer-funded retention pools (not from purchase price)

Negotiate rollover requirements

Ensure fair distribution to broader team, not just C-suite

Get buyer agreement on your critical person list early

3 Risk Mitigation:

Never make someone a closing condition unless you’re certain

Have backup plans for each critical role

Consider pre-signing retention agreements with key people

Build cushion into closing timelines for retention negotiations

Representations and Warranties

The Representations and Warranties (”Reps and Warranties”) section will likely be 30-50 pages of the purchase agreement and will include every assertion you’ve made about your business formalized into legal commitments with financial consequences for inaccuracy. Everyone on the deal team should go over every section they have knowledge about with the lawyers, ask questions, and expect many rounds of revisions. This is why you hired great lawyers. Errors here can cost millions. Get D&O tail insurance anyway. And expect to negotiate who pays the R&W Insurance premium. Generally, your buyer should procure and pay for the R&W Insurance. If your buyer refuses to pay for it, tell them you want to be involved in detail in the selection of the insurer and negotiation of their contract… the buyer will likely agree to pay to avoid this.

Final Bids and Selection (~2 Months)

Expect significant movement in the final days. Our philosophy:

Remove non-contenders early

Evaluate remaining bids against your stated objectives

Beware the buyer who increases their bid, but also their caveats and reservations

Consider objective achievement probability and timeline

Make the hard choice based on your “why”

Don’t look back

Post-Signing to Close

After signing, expect:

Public disclosure (you will have a whole host of new friends who read about your financial success… when you buy a boat, lots of folks want to ride on your boat… when you sell a company lots of folks want to help you with the fruits of your success)

Internal communication with your team (why did we do this, what does it mean for me, who is in charge, where do I go with additional questions)

Additional due diligence from the buyer

Working capital calculations (beware the buyer who views working capital as a source of incremental value)

Regulatory approvals (HSR/antitrust)

Closing condition satisfaction

Integration Planning

Closing will be both an ending and a beginning. The acquirer bought you for reasons: to integrate you into their organization because you bring something that they need, to merge the two organizations together because you’re more competitive together, or to inject resources (and oversight) to accelerate your growth. Before closing you will probably jointly create a milestone plan of what will be accomplished by 30, 60, and 90 days such as moving business systems to incorporating the policies and procedures the buyer wants for growth. The post-closing progress against this plan will probably be briefed to the board of directors so negotiate it as if the milestones are written in stone.

Timeline varies from weeks to over a year depending on complexity. Then it’s over and integration begins.

Traditional Closing Platitudes

When your deal closes, expect to hear:

“Go f* yourself”** (said laughingly) meaning you won the game, and they’re jealous

“Go make your spouse a sandwich” which acknowledges your family’s sacrifice and contribution

“You won the game” which is self-explanatory

“I have an investment idea for you”

Conclusion

This guide represents hard-won lessons from our M&A journey. Every situation differs, but these fundamentals should help you achieve better outcomes while maintaining your integrity throughout the process.

To those embarking on this journey: prepare thoroughly, choose your partners wisely, and remember that the best deal isn’t always the highest price. The best deal is the one that achieves your objectives.

Good luck. Someday, we hope to tell you to go make your spouse a sandwich.