AI Great Powers Part 5: The Trench Coat: Who Actually Pays for China’s Chip Push (It Isn’t Beijing)

Local governments out-spend Beijing’s famous Big Fund 1.31:1 (as equity, not grants) while the data-center boom runs on a different subsidy entirely: the electricity bill.

Money, it’s always money. Beijing’s “Big Fund” is the most famous industrial-policy vehicle on earth. And it is not the biggest check-writer in China’s chip push. The biggest check-writers are city governments you have never heard of, investing as shareholders so the money never reads as subsidy.

Results Up Front

This is long, and I do not expect most people to read the whole thing. Here is what the money trail says.

China subsidizes silicon with equity and data centers with electricity. Both channels sit where conventional subsidy accounting cannot see them.

Four findings carry the piece:

There is ≈US$0 of fab subsidy inside Huawei itself. Its bond documents show zero government-grant lines feeding fab construction. The money that built the “Huawei shadow fabs” sits one layer away, on balance sheets nobody audits for subsidy.

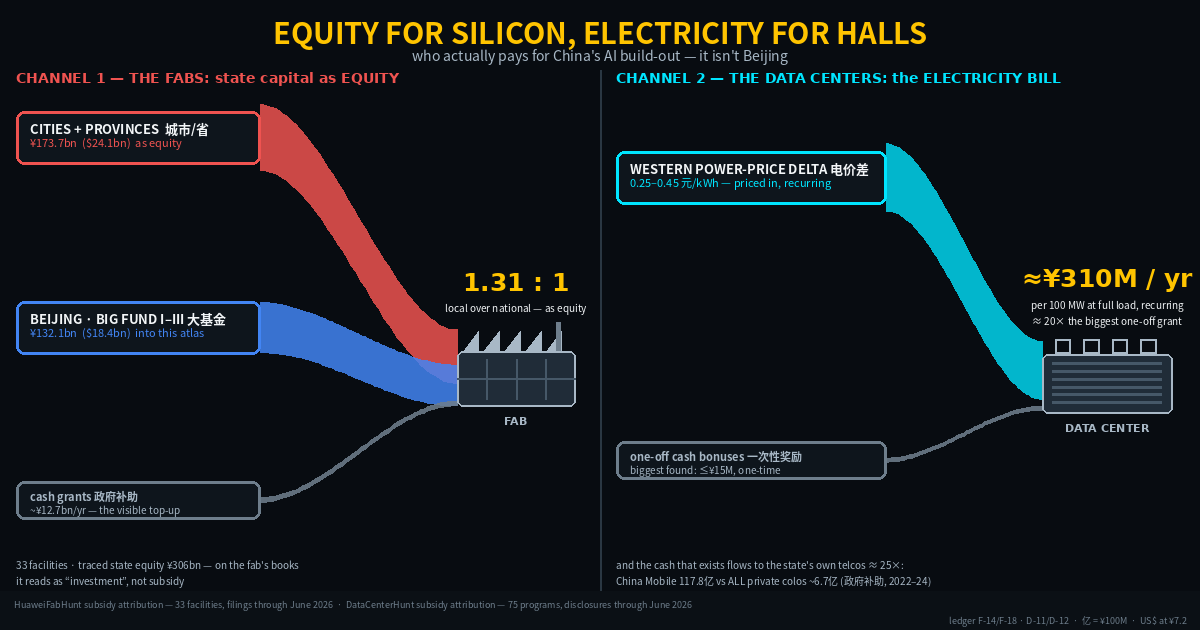

Local government out-finances Beijing. Across the 33 facilities in my atlas with traceable state capital, the national Big Fund system put in ¥132.1bn (about US$18.4bn); provinces and cities put in ¥173.7bn (about US$24.1bn), a 1.31 : 1 local-to-national ratio, and overwhelmingly as equity through municipal state-owned enterprises (SOEs), not grants. The annual grant flow, the thing that actually shows up in a P&L as “subsidy,” is only about ¥12.7bn (~US$1.8bn) a year. A top-up, not the engine.

The data-center subsidy is not cash at all. It is the electricity price. The western-hub power discount of ~0.25–0.45 yuan per kWh is worth roughly ¥310M (~US$43M) a year to a single 100 MW data center actually drawing that load, about 20× the largest one-off cash grant on offer. And it recurs, for as long as the pricing structure holds. The biggest cash numbers go to the state’s own telecom operators, at roughly 25× what the entire private colocation industry receives.

This is not one machine. It is a tournament. A dozen-plus cities making concentrated equity bets, Beijing co-investing in the ones that validate. Hefei’s city SOEs built both of Anhui’s flagship fabs. Jinjiang’s bet idles far below its power nameplate. Qingdao’s barely changed across four years of satellite frames. The wreckage is absorbed locally and quietly; the tournament keeps producing bets.

Housekeeping: USD equivalents at roughly RMB 7.2 per US$1 throughout. And every claim is time-boxed: document claims are stamped to the filing date, imagery claims to the collection date of the frame; “as of June 2026” is the series freshness stamp. A built shell is not an operating fab. Where I project, I label the projection and its confidence.

Part 4 told the story of how these facilities were found. This part follows the money that built them.

The zero that started it

The natural first place to look for the rumored US$15–20bn behind Huawei’s chip-making is Huawei. Huawei issues bonds in China, and Chinese bond prospectuses disclose government grants: the line item is called 政府补助, and auditors total it.

We read those documents. The fab-subsidy total inside Huawei is approximately zero.

Not small. Zero. Its construction-in-progress is self-funded campuses and staff housing. The company at the center of the largest state-backed chip build-out in the world shows no state money for chip-making on its own audited books.

That zero is not an absence of evidence. I read it as design: an inference, but one the rest of this piece earns.

If you want to move tens of billions into a sanctioned company’s supply chain without it ever appearing as a subsidy to that company, you do not write the company a check. You stand up new companies the sanctioned firm does not own, capitalize them with state equity one administrative layer down, and let the firm control them through everything except ownership: shared executives, guaranteed off-take, tools, co-location. The money is parked exactly where nobody audits for it.

I called this CFO camouflage in Part 1. This part is the audit.

The fab layer: the subsidy is equity

Here is the accounting mechanism, because the mechanism is the finding.

A cash grant lands on the recipient’s income statement under 政府补助. It is visible, auditable, totalable: the raw material of countervailing-duty cases. Across all the listed Chinese chipmakers in my atlas, that flow runs about ¥12.7bn (~US$1.8bn) per year (filings through June 2026). Real money. Not remotely enough to build a fab base.

Equity is different. When a municipal “guidance fund” or a city SOE buys into a fab as a shareholder (often through a limited-partnership structure with a commercial-looking general partner), the money arrives as paid-in capital. On the fab’s books it is indistinguishable from any investor’s stake. The subsidy exists only in the gap between the return the city will accept and the return a market investor would demand. And that gap appears on no financial statement anywhere.

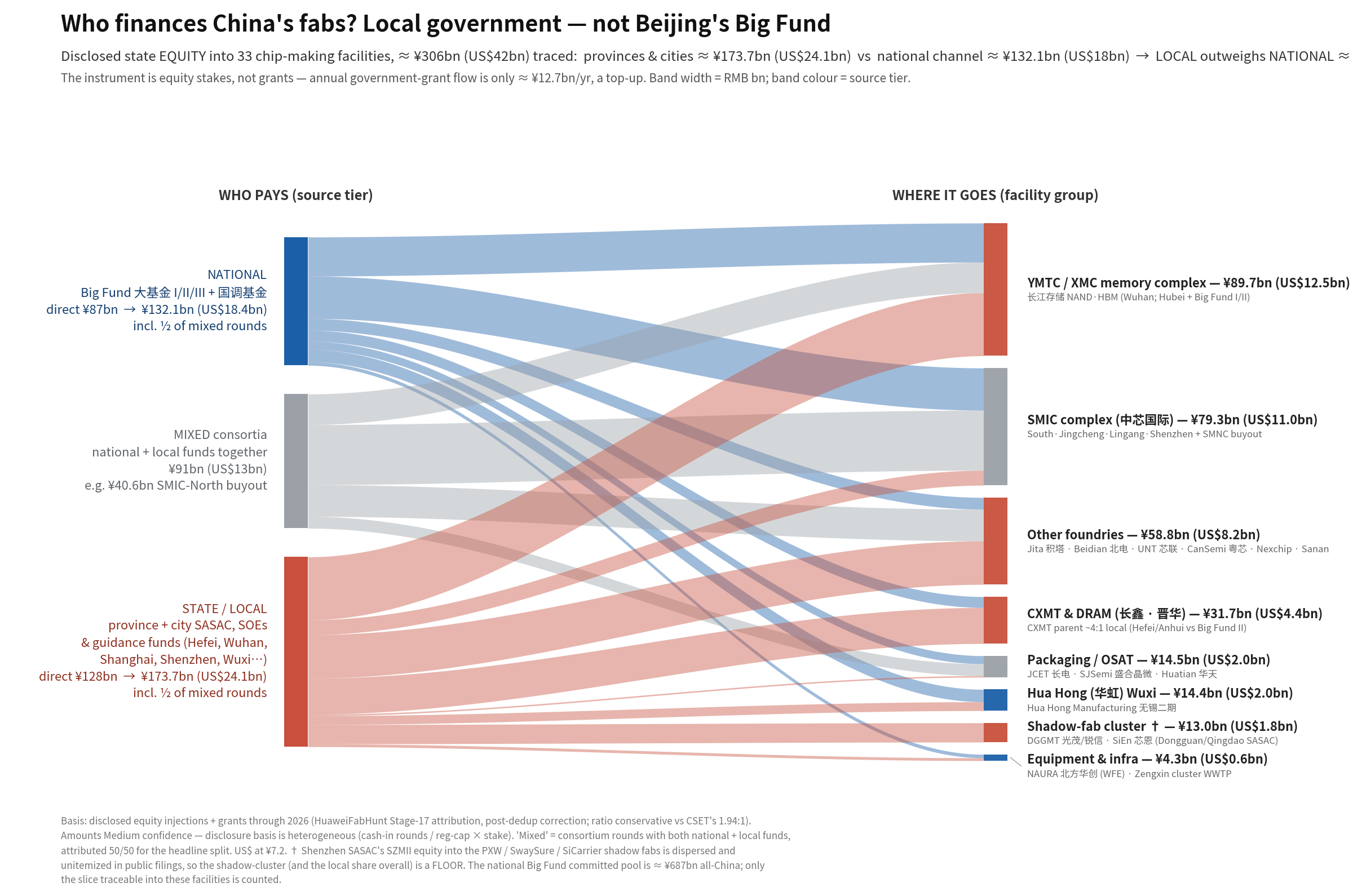

This is not fraud. It is accounting. And it works: total it up across the 33 facilities where the state capital can be traced, and the equity stock comes to roughly ¥306bn (~US$42bn): twenty-six years of the grant flow, sitting in plain sight as “investment.”

Now split that equity by who wrote it:

How to read it: left nodes are capital sources, namely national (Big Fund I/II/III + the state structural fund, blue), mixed national+local consortia (gray, split 50/50 in the totals), and state/local (province + city SASAC vehicles, SOEs, and guidance funds, red); ribbons flow rightward into eight facility groups, scaled by disclosed equity in ¥bn. What to see: the red is wider than the blue. Local capital out-finances Beijing ≈1.31:1 across these 33 facilities, and it flows as equity. Source: HuaweiFabHunt subsidy attribution, 33 facilities, filings through June 2026; amounts medium-confidence (heterogeneous disclosure basis); US$ at ¥7.2.

The national channel is the famous Big Fund (国家集成电路产业投资基金), phases I through III, plus the state structural-adjustment fund. It accounts for ¥132.1bn (US$18.4bn) of equity into the facilities in this atlas. Scope that carefully: the Big Fund’s total committed pool across all phases is roughly ¥687bn (~US$95bn), but most of it flows to design houses, tool-makers, and facilities outside this atlas, or gets recycled. The ¥132.1bn is what legibly lands on these 33 fabs.

The state and local channel is city and provincial SASACs (the State-owned Assets Supervision and Administration Commissions, the bodies that own China’s state enterprises), municipal SOEs, local guidance funds. It accounts for ¥173.7bn (US$24.1bn).

Cities and provinces out-financed Beijing 1.31 to 1.

That ratio is the load-bearing number of this article, so treat it with the respect of a confidence grade: the individual equity amounts are medium-confidence, because Chinese disclosures mix bases (cash-in rounds, registered-capital × stake, market value of stake). The ratio is robust to that noise, because both sides are computed the same way. And it is, if anything, a floor on the local side, for reasons the next section makes physical.

The trench coat

The rumor this project began with was that ~US$15–20bn of state capital stood behind Huawei’s chip network and appeared in no audited filing. I found it. It was never missing. It was unitemized.

It sits on the consolidated balance sheet of one company: Shenzhen Major Industry Investment Group (SZMII, 深圳市重大产业投资集团), wholly owned by Shenzhen SASAC. SZMII owns the equipment champion SiCarrier and the shadow fabs: SwaySure (DRAM/HBM), PXW (logic), Pensun (logic), Pengjin (SiC/GaN), with parallel structures in Dongguan (DGGMT) and Qingdao (SiEn) under their own city SASACs. SZMII’s consolidated assets grew from ¥38.9bn to ¥138.0bn between 2022 and mid-2025 (filings through 2025 H1): roughly US$13.7bn of balance-sheet growth over exactly the fab-build window. Because SZMII consolidates its operating subsidiaries, that capex never appears as an itemized line anywhere. Bottom-up, the network’s full-build implied capex is US$27–57bn: a band that comfortably contains the famous single-sourced “$30bn” figure, dominated by SwaySure’s memory build.

And Huawei’s equity stake in all of this is the same number as its subsidy line: zero. Across the whole cluster the equity column is empty. The control ties are real but ownership-free. The strongest single one is a named person: a SiCarrier director (its shareholder representative) who is simultaneously a sitting Huawei vice-president (single-sourced, but unrebutted). Add to that ex-Huawei management at PXW, near-total off-take to Huawei, and physical co-location. (Attribution of unlisted entities to Huawei is inferential; the US Entity-List rationale is the strongest public signal, and the ledger grades those linkages claim-by-claim.)

For the engineers who want the wiring diagram rather than the metaphor:

How to read it: nodes are entities, edges are equity stakes from the corporate registry; Shenzhen SASAC → SZMII → the fab and equipment subsidiaries. What to see: every path to the shadow cluster runs through municipal SASAC capital. And no edge connects to Huawei. Source: HuaweiFabHunt entity ownership map, registry filings through June 2026.

The trench coat is not Huawei wearing a disguise. It is three city governments standing on each other’s shoulders, wearing a commercial coat, building fabs around a company they conspicuously do not own.

Beijing follows; cities lead

Two more receipts pin the local-first pattern.

CXMT, China’s flagship DRAM maker and the single most strategically important memory company in the country, runs about 4 : 1 local: roughly ¥20.4bn from Hefei city and Anhui province vehicles against roughly ¥4.7bn from Big Fund II. The legible national champion is, by capital, a Hefei project. And Hefei’s city SOEs did it twice: the same municipal investment companies anchored both of Anhui’s flagship fabs: CXMT and the foundry Nexchip. Analysts call it “the Hefei model.” It is a city treating fabs the way other cities treat stadiums, except the bets are bigger and some of them pay off.

The national channel, meanwhile, behaves like a validating co-investor: it de-risks winners the locals already built. The cleanest example is the Big Fund III’s first deployment into this atlas: ¥13.19bn (US$1.832bn) into SMIC South’s leading-edge line (the line that makes Huawei’s Ascend AI silicon) in December 2025 (document date). The newest, largest national fund’s debut purchase was a deeper stake in the one fab that already worked. Beijing is not the venture capitalist in this story. Beijing is the growth-round investor.

What did all this equity actually buy? Physically: real fabs. Part 4 showed one of them going from bare earth to an operating campus in about four years. Strategically: that is Part 6’s question, and the answer is smaller than ¥306bn suggests, for reasons that have nothing to do with money.

The data-center layer: the subsidy is the electricity bill

Now walk one layer downstream, to the data centers being built to house the AI chips. (This is a companion project to the fab hunt: same method, demand side.) Ask the same question: who pays?

If you go looking for grants, you find the same misdirection as in the fab layer, with a twist. The national program everyone cites (东数西算, “Eastern Data, Western Computing,” the plan to move compute to the cheap-power west) shows more than ¥43.5bn (~US$6bn) of direct investment and over ¥200bn (~US$28bn) of leveraged mixed government-and-social capital. The largest pure-cash channel is 算力券, “compute vouchers,” worth about ¥1.97bn (~US$270M) a year across fifteen cities. And of the recurring operating-subsidy programs, about 68% are local, not central. Local again. The pattern survives the layer change.

But all of those numbers are rounding errors next to the real instrument.

The real data-center subsidy is the electricity price. Delivered industrial power in the western hubs runs about 0.32–0.40 yuan per kWh; in the eastern load centers, 0.6–0.8. That is a structural discount of ~0.25–0.45 yuan per kWh. And you can redo the arithmetic yourself. A 100 MW data center drawing its full load runs 876 million kWh a year. At a 0.35 yuan delta, that is ¥310M (~US$43M) saved, every year: roughly 20× the largest one-off cash grant we found offered anywhere (disclosures through June 2026).

The subsidy is not fiscal. It is priced in. It appears in no budget, no grant table, no WTO notification. It is simply the rate at which policy-shaped western power contracts clear. Countervailing it means proving the price itself is the subsidy: a far harder, slower case than pointing at a grant line.

And an operating subsidy does something a capital grant cannot: it keeps capacity alive. A capex grant builds a hall once, and then the hall must earn its keep or die. A power-price delta pays the hall’s dominant operating cost month after month, so an underfilled data center on cheap western China power does not go bankrupt. It idles, cheaply, waiting for chips that are coming much more slowly than the concrete did. How slowly, and how many halls are waiting: that is Part 7.

Where actual cash does flow, it flows to the state’s own. Government grants received over 2022–24: China Mobile ~¥11.78bn (117.8亿), China Telecom ~¥6.77bn, China Unicom ~¥3.34bn, against roughly ¥670M (6.7亿) for the entire independent colocation industry combined. The state subsidizes its own SOE operators at roughly 25× the private field. Conservative however you cut it: China Mobile alone is ~18× the entire private field; the three telcos together, ~33×. The private colos compete for vouchers; the telcos get appropriations.

How to read it: the left panel shows the annual saving from the western electricity-price delta for one 100 MW data center drawing its full load (shown at a 0.35 yuan/kWh delta), next to the largest one-off cash bonus we found offered anywhere (Zhongwei’s 万卡-cluster bonus, capped at ¥15M); the right panel shows government grants received (政府补助) over 2022–24, the three state telecom operators versus the entire independent colocation industry combined. What to see: the recurring kWh delta dwarfs the biggest one-off cash grant ~20× (and it repeats every year), while the cash that exists flows ~25:1 to the state’s own telcos. Source: DataCenterHunt subsidy attribution, 75 programs/instances, plus telco audited annual reports; disclosures through June 2026; US$ at ¥7.2.

Two channels, one design principle

Put the two layers side by side and the unified thesis writes itself:

Equity for silicon. Electricity for halls.

The fab layer gets patient municipal capital, because fabs are giant one-time capital problems, and equity is the subsidy that looks like investment. The data-center layer gets a structural operating discount, because data centers are giant recurring power bills, and a price is the subsidy that looks like geography.

Neither channel produces a subsidy line. A grants-first accounting of China’s AI build-out (still the default in the policy debate) captures the ¥12.7bn-a-year top-up and the compute vouchers, and misses the ¥306bn of equity and the perpetual kilowatt-hour discount almost entirely. (The careful shops do count the equity: CSET’s tally finds the same local-over-national pattern; the headlines never do.) The conventional ledger sees the tip and reports the tip.

This is not an accusation of concealment, exactly. Every government invests through state vehicles and shapes utility prices. It is an observation about instrument choice: China’s planners picked, for each layer, the one instrument that conventional subsidy accounting is structurally blind to. Twice is a pattern. Instrument choice is the observable. Intent is my inference from it.

Fragmented mercantilism: a tournament, not a machine

Here is where I part company with the standard Washington read of “Made in China 2025.”

The standard read is a machine: Beijing sets a target, money flows down, fabs come up. What the capital trail actually shows is a gambling tournament: dozens of cities nationally making large, concentrated, competing equity bets (my atlas traces the eight biggest), with Beijing arriving afterward to scale the winners. The 1.31:1 ratio is what a tournament looks like in accounting form.

Tournaments have losers, and the losers are instructive.

JHICC (Jinjiang, Fujian) was a city-and-province DRAM bet that ran into a Micron lawsuit and a 2018 US entity-listing. Big Fund II’s stake is ¥2.715bn (~US$380M). Note the figure, because my own pipeline first carried it as ¥27bn, a tenfold error the cross-check caught. The whole project’s disclosed scale is roughly ¥37bn (~US$5.1bn) committed across phases, with a 60k wafer-per-month nameplate; its 2024 revenue was about ¥1.4bn: the financial signature of a fab running far below its nameplate (filings through June 2026).

SiEn (Qingdao) was Qingdao SASAC’s bet. Across satellite imagery spanning 2022 through 2025, the campus is near-static: the build essentially stalled as of the latest frames. A shell is not a fab, and a city can buy a shell.

A unit-discipline aside, because it is part of the credibility story: the Chinese counting unit 亿 is 100 million (117.8亿 is ¥11.78bn, not ¥117.8bn), and the 亿-to-billion conversion is a tenfold error machine. I know because it claimed my own pipeline seven times: the build script for the subsidy table applies seven logged, transparent 10× corrections that were caught by cross-checking each claimed stake against percentage-times-registered-capital. (JHICC’s “¥27bn” fails that check instantly: its entire phase-one was ¥3.7bn.) Every figure in this piece has been through that check. When you see a China-subsidy number elsewhere, run it yourself.

Against the wreckage, set the wins: Hefei got CXMT and Nexchip and is now the center of Chinese DRAM. Shenzhen got the shadow cluster: Part 4’s PXW went from bare earth to an operating fab campus in just over four years of frames. Shanghai got SMIC’s leading edge. The tournament is wasteful the way venture portfolios are wasteful: most bets underperform, the winners pay for the portfolio, and, crucially, the wins recruit the next ten mayors. Hefei’s success is the advertisement that keeps the local capital coming.

So the correction to the standard read cuts both ways:

The coordination is overstated. “China spends $X on chips” implies a directed program. The reality is messier, more duplicative, and more failure-tolerant than the machine model: JHICC and SiEn are what the failure mode looks like, and the system absorbed both without a ripple.

The persistence is understated. A central program can be cut in one budget cycle. A tournament among dozens of cities, each with its own SASAC balance sheet, its own land, its own power pricing, and its own Hefei envy, has no off switch in Beijing. Sanctioning the program is hard because, in the fiscal sense Washington usually means, the program barely exists.

It is not a machine. It is an ecosystem with a venture model and no limited partners to disappoint.

What this means, by reader

If you set policy: stop sizing China’s chip push by announced grants. You will undercount it by an order of magnitude. Size it by the balance-sheet growth of municipal investment SOEs and by the structure of delivered power prices. And when you design responses, note what equity-and-electricity channels imply: countervailing duties and subsidy-notification fights aim at the instrument China conspicuously is not using. Note also what the money did not buy: capital this patient still could not purchase the binding inputs, which is why export controls bit where tariffs would not have. That export control story is Part 6’s.

If you staff the people who set policy: every number above traces to a public document, and the receipts block below carries the ledger IDs, the confidence grades, and the known weaknesses. The two artifacts to pull first: the 33-facility subsidy attribution table (fab layer) and the 75-row data-center subsidy table (DC layer). The equity amounts are medium-confidence; the local-over- national ratio and the equity-over-grants structure are the robust findings. Quote those.

If you build things: the channel predicts the build. Equity buys fabs whether or not demand has materialized, which is why China’s mature-node capacity keeps growing through a glut. Cheap electricity keeps halls standing whether or not chips exist to fill them, which is why the western China hubs keep topping out shells. Subsidy design, not demand, explains most of what you can see from orbit. And neither channel can conjure the one input that is actually scarce. What that input is, and the arithmetic that makes it binding, is Part 6.

The best arguments against this

The strongest objections I know, promoted to the body of the piece where they belong:

The equity amounts are softer than the ratio. Disclosure bases are heterogeneous (cash-in rounds vs registered-capital × stake vs market value). I grade every amount medium-confidence and defend the 1.31:1 ratio, which is computed symmetrically on both sides.

The 33-facility atlas is not all of China. Correct: ¥306bn is the traced equity, a floor. The biggest known omission cuts in my favor: SZMII’s shadow-fab equity is consolidated and unitemized, so the local side is understated.

The electricity delta is not 100% subsidy. Some of it is genuine cost difference: stranded western renewables are cheap to generate. True. But the delivered-price structure is policy-built (hub designation, mandated transmission, PPA frameworks), the delta is what actually moves builds west, and none of it appears in any fiscal account. Call it policy-shaped price geography; the accounting-invisibility point stands.

The mixed consortia could tilt the ratio. ¥90.7bn of the equity comes from consortia of national and local funds (the ¥40.6bn SMIC-North buyout is the biggest). I split mixed 50/50; the ratio stays above 1:1 unless the mixed pool is in truth more than about three-quarters national. And that biggest mixed item, the SMIC-North buyout, was a five-fund consortium with local co-investors alongside the Big Fund.

The tournament could itself be the design. Beijing sets the targets (Made in China 2025), controls the promotion incentives of every mayor playing, and operates the Big Fund as the tournament’s prize. On this reading, “fragmented” is just how a deliberately decentralized central program executes, and calling it “not Beijing” relabels rather than refutes coordination. I can’t disprove that from capital flows alone. What the money trail does establish: the capital and the losses sit on local balance sheets either way, so the persistence argument (no off-switch in a single budget) survives both readings. What changes is only how much credit Beijing gets for the architecture.

What would change my mind

As of June 2026, none of these has fired:

Itemized SZMII subsidiary accounts showing fab capex materially below the US$27–57bn implied full-build band: the trench-coat finding shrinks accordingly.

A documented Huawei equity stake in any shadow-cluster entity: the “control without ownership” architecture claim falls.

A re-attribution on better disclosure that pushes the national channel above the local one into this same atlas: the 1.31:1 headline inverts.

Western power-price reform closing the delivered delta below ~0.1 yuan/kWh: the electricity channel stops dominating the DC subsidy story.

A central cash program for private colos at telco scale: the ~25× asymmetry breaks.

One more receipt, and it is fresh: after this article was drafted, a sibling project recalibrated every equity row in this atlas against primary filings and caught three errors in mine. Two were 10x unit slips. One was a US-dollar registered capital converted as if it were yuan. Corrected, the ratio moves from 1.39:1 to 1.31:1. The direction does not move, and the finding does not move. That is what the ledger is for: when a number in this series changes, you read it here first, with the arithmetic shown.

Receipts

Load-bearing claims in this piece the ledger is on my substack. - Local ¥173.7bn vs national ¥132.1bn ≈ 1.31:1, as equity; grant flow ~¥12.7bn/yr: F-14; amounts medium-confidence (heterogeneous basis), ratio robust; mixed consortia (¥90.7bn) split 50/50; filings through June 2026. - ≈US$0 fab subsidy inside Huawei; no Huawei equity in the shadow cluster; SZMII consolidation; full-build US$27–57bn: F-15/F-16; ownership high-confidence (registry), dollar split a sourced estimate; Huawei attribution inferential, graded per claim. - CXMT ≈4:1 local; Hefei SOEs built both CXMT and Nexchip: F-17; amounts medium, pattern high. - Big Fund III debut: ¥13.19bn/US$1.832bn into SMIC South’s Ascend line, Dec-2025: F-18; scope note: Big Fund total ≈¥687bn ≠ the ¥132.1bn traced into this atlas. - JHICC ¥2.715bn (not ¥27bn) Big Fund II; ~¥37bn total; under-utilized. SiEn near-static in imagery 2022–2025: F-19; JHICC financials document-dated; SiEn stamped to frame dates. - Electricity delta 0.25–0.45 元/kWh ≈ ¥310M/yr per 100 MW ≈ 20× one-off grants; structural, not fiscal: D-11, high (price disclosures + program tables). - Telco grants 2022–24: CM 117.8亿 / CT 67.7亿 / CU 33.4亿 vs all private colos ~6.7亿 ≈ 25×: D-12, high (audited annual reports). - 东数西算 >435亿 direct / >2,000亿 leveraged; 算力券 ~19.7亿/yr; recurring subsidy ~68% local: D-13, medium-high.

Unit discipline, stated plainly because it is part of the result: 亿 = ¥100 million; 117.8亿 = ¥11.78bn. The 亿↔billion slip is a recurring 10× error in published China-subsidy figures; the build pipeline behind this piece applies seven logged 10× corrections, each caught by a percentage-times-registered-capital cross-check. USD at ~¥7.2 throughout.

Document claims are stamped to filing dates; imagery claims to collection dates; series freshness stamp June 2026. Charts: HuaweiFabHunt subsidy attribution (filings through June 2026) and entity ownership map (registry, June 2026); DataCenterHunt subsidy attribution (disclosures through June 2026). Part 4: how the facilities were found. Part 6: what the money has and hasn’t bought. Part 7: the halls the electricity keeps standing.