AI Great Powers Part 2: Chinese Model Builders

China can still build under sanctions. What it can’t yet match is America’s private hyperscaler capex light-money-on-fire hose.

Part 1 was the supply-side story.

It asked whether China can keep building AI hardware after the United States tried to choke off the easy path.

The answer was yes, but not for free. China can build. It can route around some of the damage. It can use Huawei, SMIC, domestic equipment makers, chip startups, state funds, and a lot of brute-force systems engineering. But the bottleneck is memory, and the tax shows up in cost, power, friction, and uncertainty.

This is the capital-deployment story that Chinese companies report in their English language filings. Yes, this two part story has at least a third part on the difference between English language and Chinese language filings; I’m writing this before I have dug in to the Chinese language ones to isolate my biases.

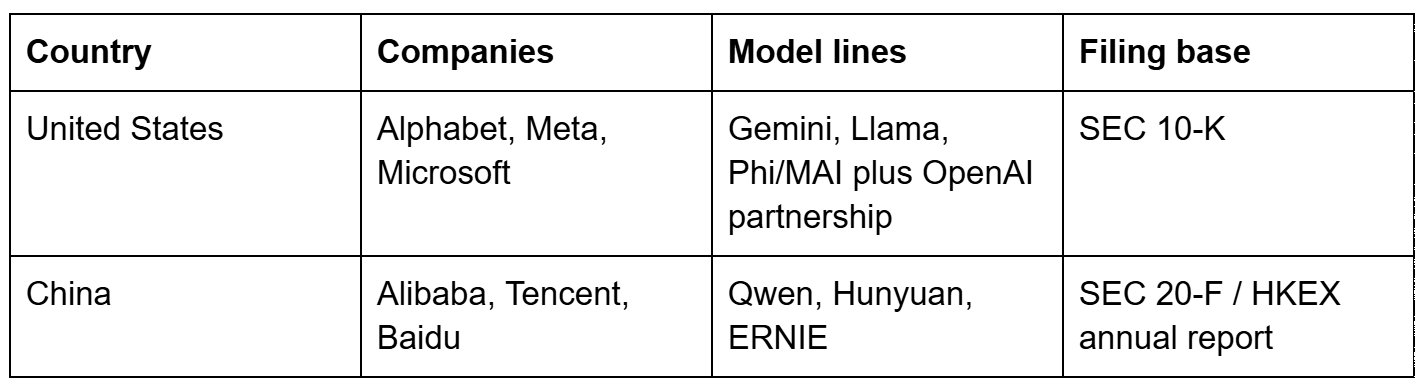

If China can build increasingly domestic AI hardware, are Alibaba, Tencent, Baidu, ByteDance, and iFlytek spending on AI like Alphabet (Google), Meta (Facebook), and Microsoft?

No.

And that no matters.

Not because Chinese AI is fake. It is not. Qwen, DeepSeek, Hunyuan, ERNIE, Doubao, and Spark are real products backed by real companies. Alibaba’s Qwen in particular keeps showing up in the global open-weight conversation for a reason.

Part 1 showed that China can keep building under constraint. It did not show that China has the same private-sector capital engine as the United States.

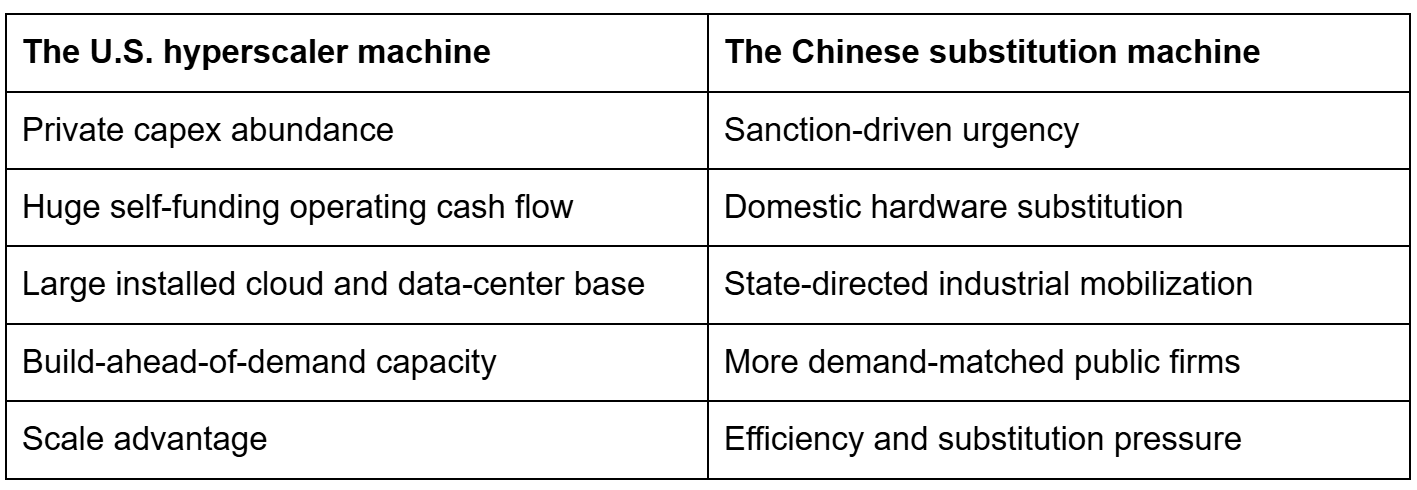

The filings show a different kind of contest. America has a private-sector hyperscaler capex machine of astonishing size. China has a national mobilization under constraint. Both are powerful. They are not the same thing.

Results Up Front

This is long, and I do not expect most people to read the whole thing. The rest of the post tells you how I got here. The research data was current as of June 4, 2026.

The strategic version is this:

The AI hardware contest is not just a chip contest. It is also a capital-deployment contest. On that dimension, the United States has a private-sector advantage that the Chinese public model builders do not match. Alphabet, Meta, and Microsoft are not just buying more infrastructure. They are funding a geopolitical compute position from gigantic internal cash engines.

The strongest evidence is now filing-grade. Alibaba’s FY2026 20-F and Baidu’s FY2025 20-F are already on EDGAR (SEC’s Electronic Data Gathering, Analysis, and Retrieval (EDGAR) system). Tencent and iFlytek have filed FY2025 annual reports. The three U.S. hyperscalers have filed FY2025 10-Ks. So the latest China-public-company conclusion does not rest on press releases. The notable exceptions are Hangzhou (DeepSeek) and ByteDance, because they are still private companies.

Inside the audited set, the private-capital gap is huge. Alphabet, Meta, and Microsoft spent about $225.7 billion of capex in FY2025. Alibaba, Tencent, and Baidu spent about $26.1 billion. That is an 8.7x gap. The U.S. trio also had about $416.7 billion of operating cash flow versus $65.4 billion for the China trio, and about $628.0 billion of net PP&E (Property, Plant, and Equipment) versus $53.2 billion. The U.S. side is buying more infrastructure, has a more substantial profit generating machine to keep buying, and starts from a much larger installed base.

Alibaba is accelerating, and that matters. Its capex rose from about $4.4 billion in FY2024 to $11.8 billion in FY2025 and $18.3 billion in FY2026. But the strategic comparison is still brutal: Alphabet spent $91.4 billion, Meta spent $69.7 billion, and Microsoft spent $64.6 billion in FY2025. Alibaba is the clearest public Chinese buildout story, and it is still not spending like a U.S. hyperscaler. There is a joke in there about scalers with Chinese characteristic but apparently I lost my sense of humor while reading financial filings until past midnight.

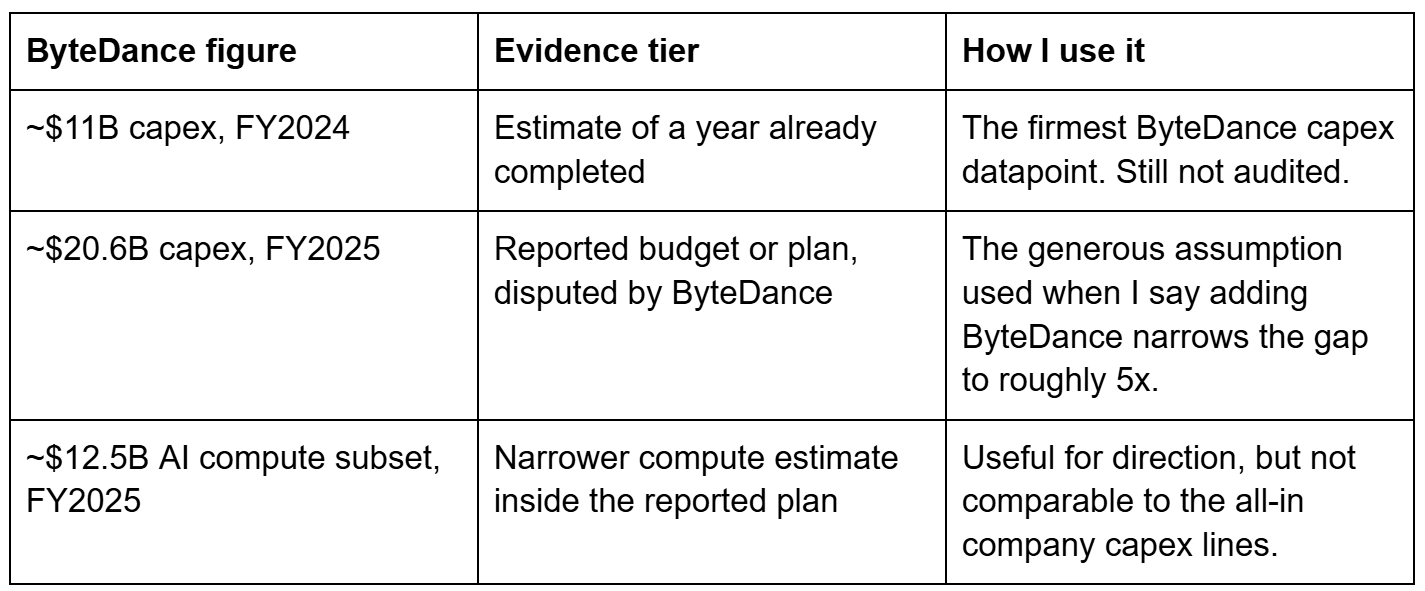

ByteDance is the important private caveat, not the refutation. The generous ByteDance assumption is a disputed FY2025 capex plan around $20.6 billion, much of it AI-related. Add that estimate and iFlytek to the China side and the gap narrows to roughly 5x. But the ByteDance number is not audited, is a plan rather than a completed result, and still does not reach Microsoft, Meta, or Alphabet. See the ByteDance box below before treating it like a filing. And the published DeepSeek numbers are too spurious to draw conclusions from.

This is a narrower claim than “China is not spending.” China has state compute funds, telecom operators, provincial data-center projects, Huawei, military demand, and a domestic-substitution machine outside this company set. The claim here is about Chinese model builders and cloud companies in public reporting, plus the best-known private ByteDance estimates. In that set, China is not matching U.S. hyperscaler private capex.

The geopolitical inference is abundance versus constraint. The U.S. has the richer private capital engine. China has the more urgent substitution engine. If frontier capability continues to depend heavily on raw compute, the filings imply a structural U.S. advantage. If Chinese labs can sustain a large capability-per-dollar advantage through efficiency, distillation, open-weight leverage, and domestic hardware substitution, the capital gap matters less than it looks. That is the real uncertainty.

The corrected mental model is not “America has everything and China has nothing.” It is also not “China has caught up.” It is a competition between an American abundance machine and a Chinese constraint machine. Both are great-power systems. They produce different investment patterns.

How to read ByteDance

ByteDance is private. It does not file audited financials. The numbers in this article are press and analyst estimates, and the estimates are not evidence.

So ByteDance matters twice. It is probably China’s most aggressive AI infrastructure spender. It is also the only large number in the comparison that is not filing-grade.

What I Measured

The question I wanted answered was narrower than the usual AI geopolitics argument:

What can we infer about Chinese AI model investment from financial reporting?

That constraint matters. I am not trying to rank model quality. I am not trying to infer secret GPU counts. I am not trying to measure every state subsidy or every provincial data-center project. I am asking what the companies themselves, and their audited or published financial reporting, say about the scale of investment behind the model builders.

The audited comparison set is:

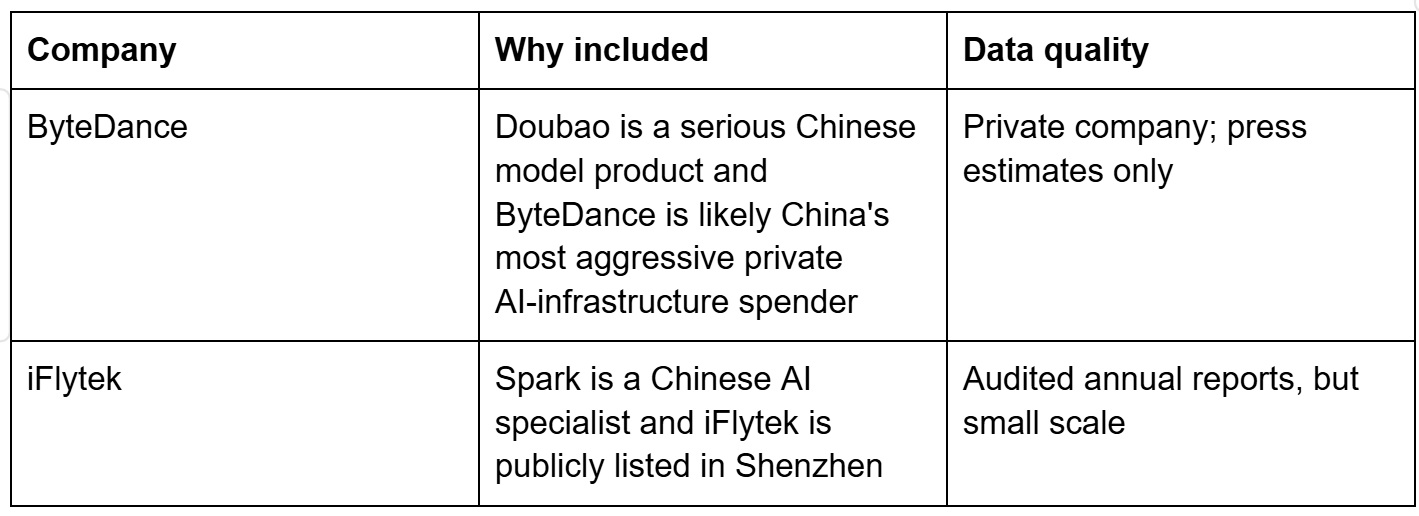

Then I added two Chinese edge cases because excluding them would make the argument less honest:

Why no DeepSeek? There was no financial reporting to draw from.

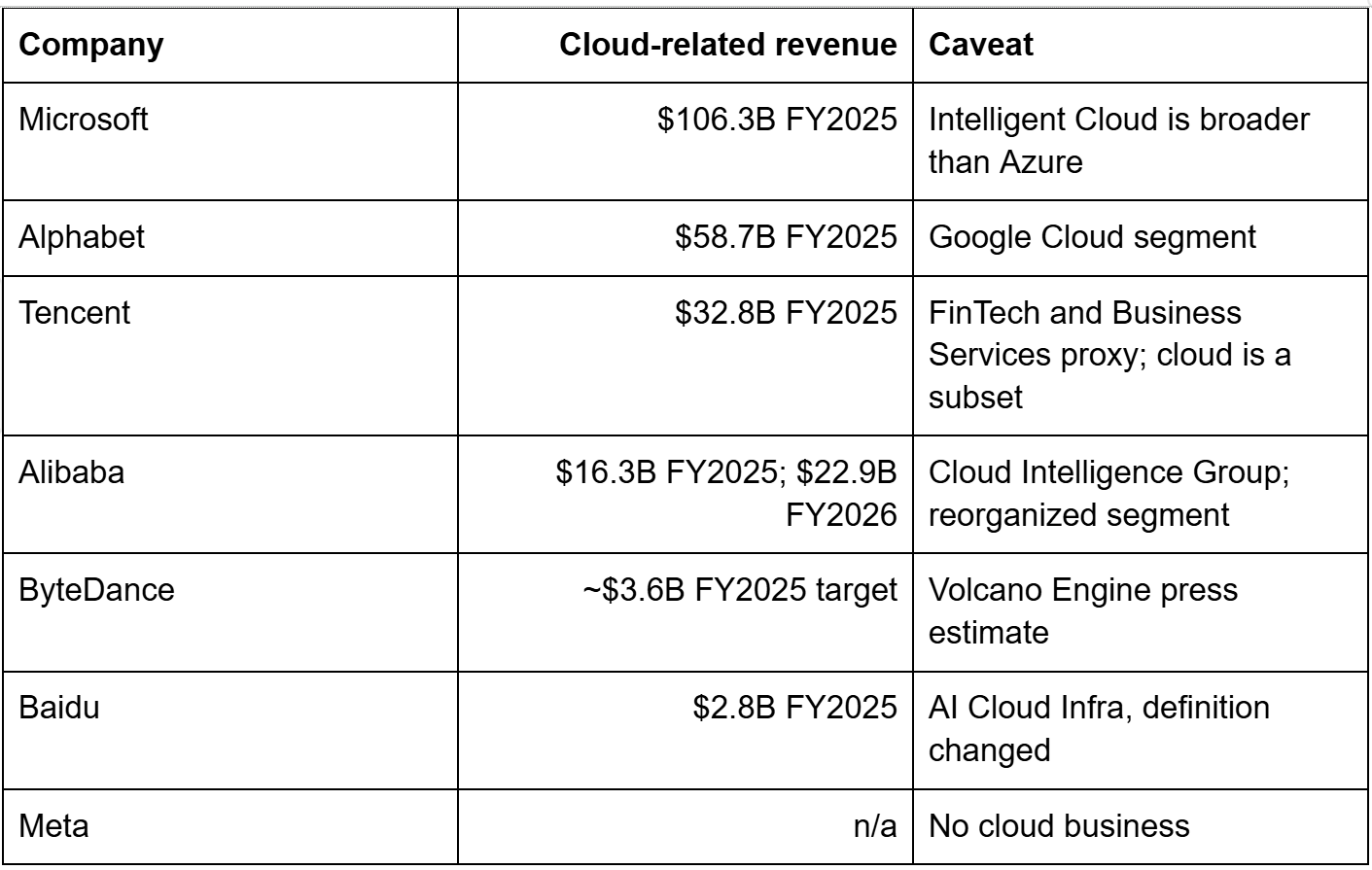

The core metrics were revenue, capital expenditure, R&D, operating cash flow, PP&E, and cloud-segment revenue where available. Capex is not pure AI capex. It includes data centers, servers, networking, offices, and other long-lived assets. R&D is company-wide, not model-only. Cloud revenue is definitionally messy because the companies do not report identical segments. Microsoft Intelligent Cloud is broad. Tencent’s FinTech and Business Services segment is only a proxy because Tencent does not break out cloud revenue cleanly.

That messiness does not make the result disappear. It actually makes the capex gap harder to dismiss, because several Chinese capex definitions are broader than the U.S. “purchases of property and equipment” line. Alibaba’s historical capex includes land-use rights and, in some years, intangibles. Tencent and iFlytek use broader long-term-asset cash-flow lines. If anything, the pure compute gap is probably larger than the reported capex gap.

How to read the numbers

Fiscal years are labeled by fiscal-year end. Alibaba ends in March. Microsoft ends in June. The others end in December.

Currency is USD where the company reports or translates to USD. RMB-only lines use filing-grounded year-end conversion.

Capex is company-level infrastructure spending. It is not AI-only capex. No company gives that line.

Cloud definitions do not match. Microsoft Intelligent Cloud is broad. Tencent’s FBS line is a proxy, and cloud is only a subset.

ByteDance is private and press-estimated. It is not part of the audited trio-vs-trio aggregate.

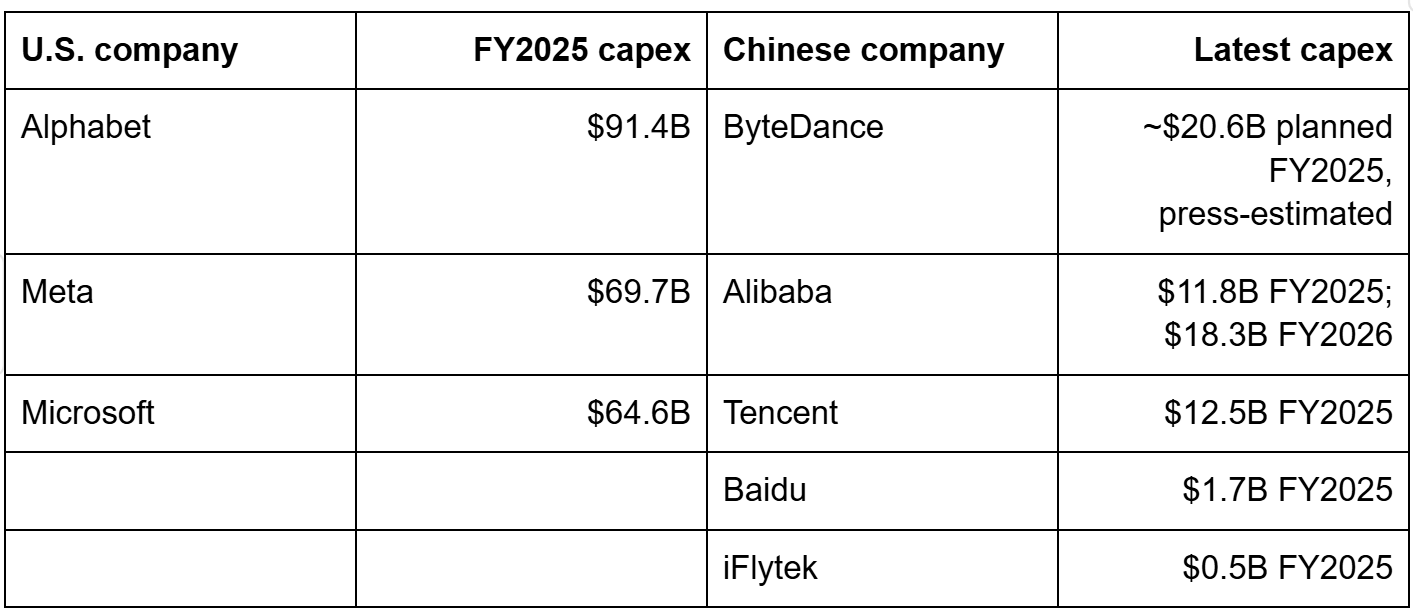

The Headline Table

Here is the latest-year capex picture.

This is the part of the story that is hard to unsee.

No single Chinese model builder matches any single U.S. hyperscaler. The closest is ByteDance, and ByteDance is the softest data point because it is private and the FY2025 figure is a reported plan, not an audited result. Even if the ByteDance estimate is directionally right, it is still about one-third of Microsoft’s FY2025 capex and less than one-quarter of Alphabet’s.

Alibaba is the most important public Chinese comparison because Qwen matters and Alibaba now gives us an audited FY2026 20-F (remember, its fiscal year ended in March). Its capex fell to about $4.4 billion in FY2024, then rose to $11.8 billion in FY2025 and $18.3 billion in FY2026. Alibaba Cloud revenue moved from about $11.2 billion in FY2023 to $22.9 billion in FY2026, though the FY2024 reorganization into Cloud Intelligence Group makes the later segment broader. The funding side moved the other way. Alibaba operating cash flow fell from about $22.5 billion in FY2025 to about $11.1 billion in FY2026 while capex rose. So Alibaba is leaning in. It is leaning in from a smaller base, with a thinner cash cushion, against U.S. peers that spend far more and fund the buildout with much larger operating cash flow.

But the question is not whether Alibaba is serious. The question is whether Alibaba is spending like Google or Meta.

It is not.

Finding 1: The Gap Widened During The AI Buildout

The common rescue for a smaller current number is trajectory. Maybe China started later and is catching up quickly.

That is not what the audited trio data shows.

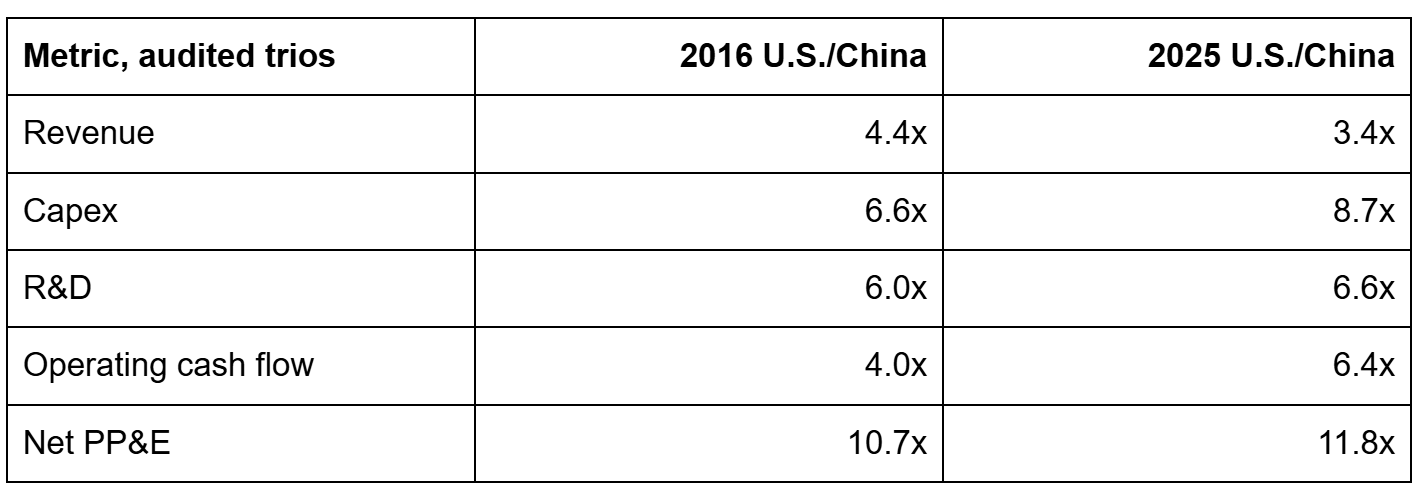

The U.S.-over-China capex ratio was about 6.6x in 2016, 5.0x in 2020, 9.2x in 2023, and 8.7x in 2025. The gap did not compress during the generative-AI era. It widened.

That matters because 2023 through 2025 is exactly when the frontier model race became a capex race. It is the ChatGPT shock, the data-center land rush, the GPU supply scramble, the power-contract scramble, and the moment every board started asking whether the company had an AI strategy.

The U.S. hyperscalers responded by turning the capex dial much harder. China responded too. Alibaba and Tencent both accelerated after their 2022-2023 lull. But the U.S. response started from a larger base and grew faster off that base.

The same pattern appears across the other scale measures:

Revenue is the important denominator. The U.S. revenue gap is large, but not 8.7x. The capex gap is much larger than the revenue gap. That means this is not just “bigger companies spend more.” It is “bigger companies are also spending harder.”

Finding 2: Normalizing By Revenue Does Not Rescue China

Capex intensity is the cleaner way to ask whether the companies are behaving differently.

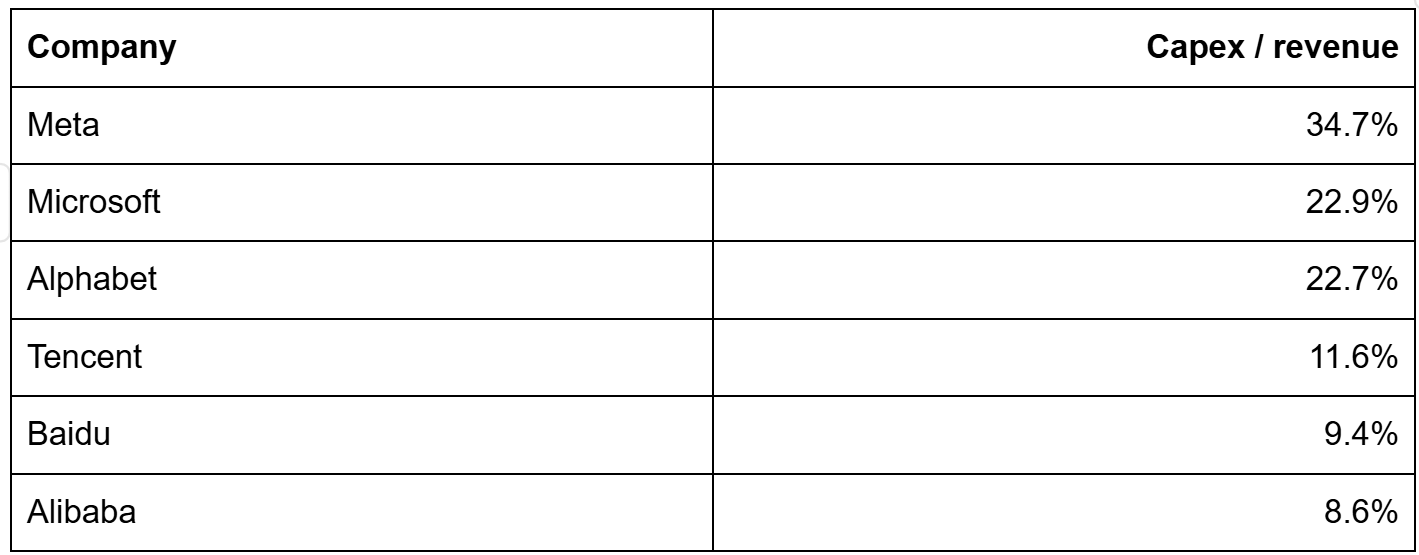

In FY2025:

The U.S. companies are spending roughly 23 to 35 cents of every revenue dollar on capital expenditure. That’s called betting the farm. The audited Chinese companies are spending roughly 9 to 12 cents.

That is the “not just scale” result.

Alibaba’s FY2026 intensity moves higher, to about 12.3%. That is a real shift. It puts Alibaba closer to a cloud buildout footing than it was in FY2023 or FY2024. But it still does not put Alibaba near Meta’s FY2025 34.7%, or Alphabet and Microsoft around 23%.

There is an alternate universe where the result looks different. If Alibaba had lower revenue but similar capex, intensity would look stronger. If Baidu were still investing like a future frontier cloud platform instead of a constrained AI software/cloud player, China would look stronger. If Tencent disclosed a much larger pure-cloud capex line, the interpretation might change.

That is not the universe in the filings.

Finding 3: A Capex War Is Also A Cash-Flow War

Capex is not just ambition. It is funding.

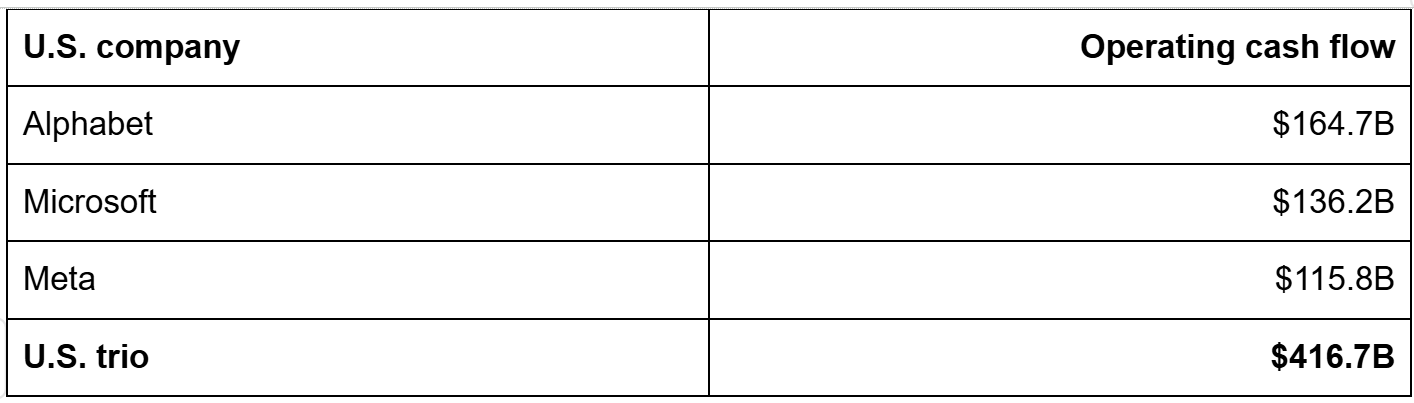

In FY2025, the U.S. trio generated:

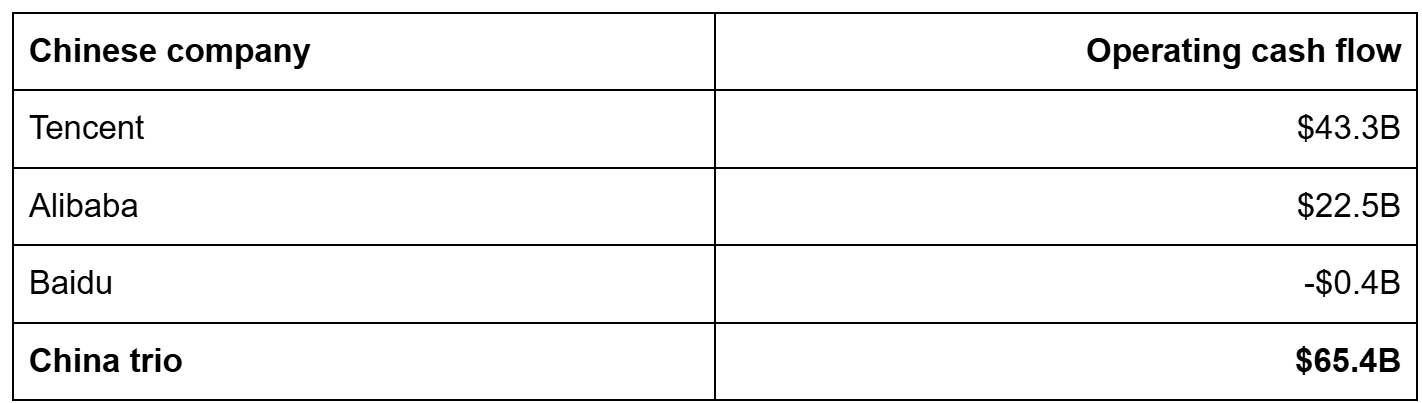

The audited China trio generated:

That is a 6.4x operating-cash-flow gap.

This is the part that makes the U.S. buildout more durable. Alphabet, Meta, and Microsoft can spend absurd amounts and still fund most of it internally. They can disappoint investors for a few quarters and keep building because the underlying cash engines are enormous.

China’s public AI/cloud companies have much less room. Tencent is the strongest cash generator in the China set. Alibaba is large but its FY2026 operating cash flow fell to about $11.1 billion, while capex rose to about $18.3 billion. Baidu’s FY2025 operating cash flow was negative.

If the AI race requires several years of front-loaded infrastructure spending before the returns are obvious, the side with the larger self-funding engine has a structural advantage.

Finding 4: PP&E Is The Accumulated Scar Tissue

Capex is the yearly flow. PP&E (Property, Plant, and Equipment) is the infrastructure stock that remains on the balance sheet.

This is the harshest chart in the project.

In FY2025, Alphabet, Meta, and Microsoft had about $628.0 billion of net property and equipment. Alibaba, Tencent, and Baidu had about $53.2 billion.

That is 11.8x.

PP&E is not a perfect compute measure. It includes buildings, land improvements, network infrastructure, leasehold improvements, and other physical assets. Depreciation policies differ. Fiscal years differ. Chinese capex definitions are not identical to U.S. definitions.

But PP&E is directionally important because AI infrastructure is not a one-year decision. It is cumulative. Data centers, power systems, server fleets, networking, cooling, and campuses become the base from which the next year starts.

The U.S. hyperscalers did not start the generative-AI era from zero. They started with a cloud and data-center base built over more than a decade. Then they accelerated.

China’s public AI/cloud companies are building too. But they are building from a much smaller installed base.

Finding 5: ByteDance Is The Important Caveat

ByteDance is the hardest company in the whole analysis because it is probably the most important Chinese AI infrastructure spender and the least transparent one.

The private-company estimates say ByteDance had about $155 billion of revenue in FY2024, about $11 billion of capex in FY2024, and a reported FY2025 capex plan around $20.6 billion. A separate estimate puts the AI compute subset around $12.5 billion. Volcano Engine, ByteDance’s cloud business, is much smaller than the capex line, with reported 2025 target revenue around $3.6 billion.

If those numbers are directionally right, ByteDance is the Chinese player that most resembles Meta: a first-party AI and consumer-app company spending ahead of a directly reportable cloud revenue line.

That matters.

It also does not overturn the result.

The generous read is to use the disputed FY2025 plan, not the firmer FY2024 estimate. That gives ByteDance about $20.6 billion of capex. Even then, it remains below Microsoft at $64.6 billion, Meta at $69.7 billion, and Alphabet at $91.4 billion. It roughly doubles the China-side capex aggregate, but because the U.S. base is so large, the China-plus-ByteDance gap still sits near 5x.

The honest way to use ByteDance is as an upside caveat on the China side:

China’s AI infrastructure spending is larger than the audited public-trio filings alone imply, because ByteDance is real and private.

But the stronger claim, that China’s model builders are matching U.S. hyperscaler capex, still is not supported.

Finding 6: iFlytek Proves Breadth, Not Scale

iFlytek is the opposite caveat.

It is public. It is audited. It has an AI model line in Spark. It is exactly the kind of specialist that should be included if the question is “who are China’s AI model companies?”

It also barely moves the aggregate.

In FY2025, iFlytek had about $3.9 billion of revenue, $0.45 billion of capex, and $0.63 billion of R&D. That is serious for a specialist company. It is not material against Alphabet, Meta, Microsoft, Alibaba, Tencent, or ByteDance.

iFlytek is useful because it keeps the China story from collapsing into only the internet giants. It shows the ecosystem has more breadth than Alibaba/Tencent/Baidu. But it does not solve the capex-scale problem.

Finding 7: Cloud Demand Is Not The Whole Explanation

The cloud-revenue comparison is where the story gets more interesting.

If U.S. companies were spending more only because they had proportionally larger cloud businesses, the capex gap would be less strategically interesting. It would mostly be a cloud-demand story.

That is not what the data shows.

Latest cloud-related revenue:

Google Cloud is about 3.6x Alibaba Cloud on the FY2025 comparison. The audited U.S.-China capex gap is 8.7x. The cloud gap is large, but it is not capex-gap large.

That points to two spending archetypes.

The first archetype is cloud resale. Alphabet, Microsoft, Alibaba, Tencent, and Baidu build infrastructure that can be sold through cloud products. This is the demand-matched model. Chinese public companies look much closer to this pattern. The cloud business grows, capex follows, and the company tries not to get too far over its skis.

The second archetype is first-party AI betting. Meta has no cloud business and still spent $69.7 billion in FY2025 capex. ByteDance, if the estimates are right, is also spending far ahead of Volcano Engine revenue because Doubao, TikTok, recommendation systems, ads, video, and internal AI products are the real demand.

This distinction cuts across countries. Meta and ByteDance look more similar to each other than either looks to a conventional cloud-resale business.

But the scale still does not cut across countries. Meta’s first-party bet is much larger than ByteDance’s reported first-party bet.

Finding 8: Disclosure Is Not Dollars

The filings also say something useful about narrative.

In FY2025, the U.S. filings averaged about 29 AI-related terms per 10,000 words. The Chinese filings averaged about 13. But the loudest Chinese filer was not the biggest spender. Baidu talks constantly about ERNIE, PaddlePaddle, Apollo, chips, and the full-stack AI story. It also spent about $1.7 billion of capex in FY2025 and had negative operating cash flow. It kind of makes me wonder if there is some partnership between Baidu and the Chinese government for state-funded CAPEX. But I have found zero data to support that conjecture. Maybe the Chinese language filings analysis will turn that up; regardless, they’re not telling English speakers.

Alibaba and Tencent talk less loudly and spend more. The business point is simple: do not confuse the AI story a company tells in a filing with the AI infrastructure it funds.

What The Data Does Not Prove

This project has a hard boundary.

It measures company-level financial reporting. It does not measure AI-only capex. No company gives investors a clean line called “frontier model training and inference infrastructure.” The capex line includes cloud resale, internal AI, offices, networks, land, leases, and ordinary business infrastructure.

It does not measure state support cleanly. China’s AI hardware mobilization includes subsidies, policy direction, state funds, local-government support, power allocation, procurement pressure, and national champions. Some of that shows up inside company filings. Much of it does not.

It does not measure capital efficiency. Qwen can be strong relative to Alibaba’s capex. DeepSeek can produce a model-quality shock at much lower apparent spend. Chinese labs may be getting more model capability per dollar through distillation, engineering discipline, cheaper labor, lower margins, more open-source leverage, or simply better choices. Financial filings cannot answer that.

It does not measure the whole Chinese AI ecosystem. DeepSeek is not in this company set because the project is financial-reporting driven. Huawei is Part 1 supply-side infrastructure. State labs, universities, government cloud procurement, and provincial compute centers are outside the audited model-builder comparison.

It does not make U.S. capex pure AI. Alphabet and Microsoft spend for cloud customers as well as internal AI. Meta spends for AI, ranking, recommendations, video, ads, Reality Labs support infrastructure, and whatever else its data-center fleet supports. The U.S. capex firehose is not a single-purpose LLM line.

It also does not make ByteDance filing-grade. ByteDance is private. Its numbers are press estimates. The FY2025 capex number is a plan, not an audited result, and ByteDance reportedly disputed some reporting around the scale of spending. I include ByteDance because excluding it would be misleading. I do not treat it as equivalent to audited filings.

Those caveats are real.

They narrow the claim.

They do not erase it.

The narrow claim is the strong one: in their public financial reporting and in the best available private-company estimates, Chinese AI model builders and cloud companies are not deploying private capital at U.S. hyperscaler scale. That is a statement about this company set, not every yuan China spends on compute.

What Would Change My Mind

This conclusion is falsifiable. Four kinds of evidence would move it.

First, audited ByteDance numbers could change the private-company side. Not one disputed budget. A few years of verified ByteDance capex in the $40 billion-plus range would make the China side look different.

Second, clean AI-compute disclosures from the Chinese public companies could show that the company-level capex proxy is missing a much larger AI buildout. Right now the capex definitions cut the other way: several Chinese lines are broader than the U.S. PP&E-purchase line, which makes the reported gap look more conservative, not less.

Third, state or provincial compute could be substituting for private model-builder capex at much larger scale than the filings can see. Some of that almost certainly exists. The question is whether it is large enough, accessible enough, and frontier-relevant enough to offset the private-capital gap. It might explain the disparity between Baidu’s claims and their audited financials.

Fourth, Chinese labs could have a durable capability-per-dollar advantage. If open-weight leverage, distillation, better engineering, synthetic data, or domestic hardware optimization lets Chinese model builders offset an 8-to-12x capital gap, then capex is still true but less decisive.

The first two would say the measurement is missing dollars. The second two would say the dollars are the wrong strategic variable. I take both possibilities seriously.

What I Now Believe

Part 1 showed that China can keep building under constraint.

Part 2 shows that the public model builders are not funding compute at U.S. hyperscaler scale.

China can be an AI Great Power without matching America’s hyperscaler capex scale. A great power can take the punch and keep building. China is doing that. The domestic hardware stack is constrained but real. The substitution machine is moving. The model ecosystem is not fake.

But scale still matters.

The United States has a private-sector capital engine that is hard to overstate. Alphabet, Meta, and Microsoft can collectively spend more than $225 billion of capex in a year, generate more than $416 billion of operating cash flow, and keep going. Their installed infrastructure base is already enormous. Their cloud businesses either fund the buildout directly or, in Meta’s case, the advertising cash engine funds a first-party AI bet at hyperscaler scale.

China’s public model builders are operating under a different constraint set. Alibaba is accelerating, but from a much smaller base. Tencent is strong, but more demand-matched. Baidu talks like an AI company but does not spend like a hyperscaler. ByteDance is the aggressive private exception, but even the aggressive estimate does not reach the U.S. companies. iFlytek adds breadth, not scale.

The result is not “China loses.”

That is too clean, and clean stories are usually where the data starts to get interesting.

The result is that the two sides are optimizing under different regimes.

Both columns are great-power advantages. They are not the same advantage, and they do not create the same investment pattern.

The strategic question is which machine matters more at which layer of the AI stack.

If frontier model capability keeps scaling mostly with compute and capital, the filings imply a structural U.S. advantage. The U.S. side is buying more infrastructure, faster, with more cash behind it, and from a much larger installed base.

If capital efficiency, model compression, open-weight diffusion, synthetic data, distillation, and domestic hardware substitution matter more than the simple capex view implies, China can remain highly competitive without matching the spending line. That is the world where Part 1’s supply-side story carries more weight.

I would not bet on either extreme.

The filings say the private-capital contest is not close.

Public model performance outside these filings, including Qwen and DeepSeek, makes it hard to treat the capability contest as settled.

That is the uncomfortable middle. China is capable. It is building. It is not matching the American hyperscaler capex light-money-on-fire hose. The U.S. has the deeper private-sector capital engine. China has the more urgent domestic-substitution machine.

The AI hardware contest is not “America has all the chips and China has none.”

It is also not “China has caught up.”

It is a competition between abundance and constraint.

That is the mental model I am carrying forward.