AI Great Powers Part 10 The Export-Control Scorecard: What Worked, What Leaked, and What to Watch

After nine posts of counting China’s chips, I owe the policy people an honest report card: not “are export controls working?” but “which ones, on what, and how do we know?” The dataset that found the hidden fabs grades the controls too, and the grades are not what either side of the argument wants.

Bottom line up front

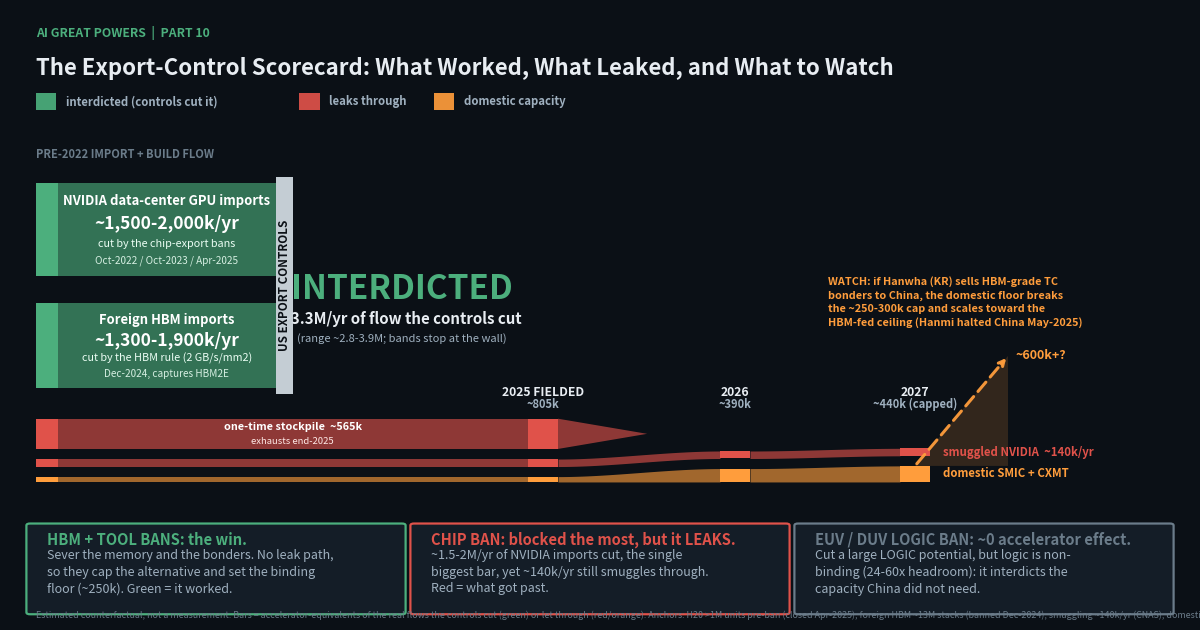

Five-plus years of US export controls, graded against what China actually built rather than the press releases, come out like this. The controls aimed at memory and at the tools that make memory created China’s binding constraint. The December 2024 ban on high-bandwidth memory (HBM, the stacked DRAM every serious AI accelerator must be packaged with) and the mid-2025 halt of Korean HBM-grade bonders are, traceably, why China’s 2026 accelerator output is capped at roughly 225k 910C-equivalents (P10–P90, the 10th-to-90th-percentile band: 192–270k), the ceiling Part 6 derives. The controls aimed at chips leaked at scale, through three mechanisms: anticipatory stockpiling (roughly 2.9 million TSMC-fabbed Ascend dies banked before each rule could bite), a deliberate carve-out (over a million legal NVIDIA H20s before the channel closed in April 2025), and smuggling (~140k advanced NVIDIA chips a year: real, bounded, not decisive). And the lithography everyone argues about was barely controlled at the level that mattered: roughly 90 immersion scanners shipped in 2024 alone. That is part of why logic capacity is not China’s problem.

The pattern in the grades is the finding. The controls that bit run through allied chokepoints (Korean bonders, Dutch scanners, Japanese tools), not primarily through hardware the United States makes. The durability of the one regime that demonstrably works is an alliance-management problem, not a rule-writing problem. As of June 2026 there is already a wobble to watch.

It is the series’ last analytical post, so it ends as the method demands: a falsifiable watch list, graded quarterly, in public.

Every claim here is time-boxed: imagery claims are stamped to the collection date of the frame, document claims to the filing date, and “as of June 2026” is the series freshness stamp. A built shell is not an operating fab. Where I project, I label the projection and its confidence.

How to grade a control

This series spent nine posts building the scoreboard most export-control arguments never keep: a facility-by-facility atlas of China’s AI-hardware capacity, a 17-claim adversarially-verified ledger (zero refuted), and one headline number. That number is the domestic accelerator ceiling, set by memory, not logic (Part 6 owns the arithmetic).

That gives a clean grading rule. A control worked if a causal chain runs from the rule to a measured constraint in the atlas. A control leaked if the prohibited thing shows up anyway (in teardowns, customs aggregates, the installed base) at a scale that mattered. Not “did China complain,” not “did revenue drop.” Did the physical buildout bend.

Graded that way, the scorecard splits down one line. Not the line between hawks and doves. The line between memory and everything else.

What worked: the memory and tool controls

The rule. The October 2022 package opened the modern era (sweeping controls on advanced logic, memory tools, and US persons), but the memory-specific bite came two years later. In December 2024, US controls banned HBM exports to China above a memory-bandwidth-density threshold (2 GB/s/mm², a line that captures HBM2E itself and everything newer), effective December 31, 2024. In May 2025, Hanmi Semiconductor, the Korean firm holding roughly 90% of the HBM3E-grade thermo-compression bonder market (TCB: the precision die-stacking tool that welds HBM stacks together under heat and pressure), halted TC-bonder shipments to Chinese customers under reported US pressure. Memory itself, and the one tool that gates making memory, cut off within six months of each other.

Why the tool half bites so hard, mechanically. A lithography ban is slow poison: China spent 2019–2023 importing more than 400 deep-ultraviolet (DUV) scanners, plus roughly 90 ArF-immersion tools in 2024 alone, so a cutoff leaves a fleet that runs for years on stockpiled spares. A bonder ban is the opposite case. China had no installed fleet of HBM-grade bonders to coast on. HBM stacking is a young step, and the yield discipline (known-good-stacked-die yield, KGSD: the fraction of finished stacks that test healthy, where one cold joint scraps the whole stack) lives in the vendor’s process recipes and field service as much as in the machine. Cut the vendor off and you don’t degrade an existing capability; you prevent one from being born. The same logic (service and spares are the real dependency) is why this project found that seizing the foreign-owned fabs on Chinese soil adds approximately zero AI compute: they decay within months once foreign service stops. And the 2026 BIS (US Bureau of Industry and Security) site-license regime that replaced the expired VEU authorizations (revoked effective December 31, 2025) now freezes those fabs at their current nodes by rule.

The measured consequence. Every downstream link is independently observable; as of June 2026 all point the same way. China’s #1 DRAM maker, CXMT, filed a STAR IPO prospectus (December 2025, cleared May 2026) that discloses no HBM product line at all: DDR4 through LPDDR5 plus a forward R&D bucket; HBM is pre-revenue at the one company expected to supply it; HBM3 mass production has slipped to late-2026/2027, production yield reported below 50% (CN-sourced, June 2026). The domestic bonder challengers (Naura, Maxwell, U-Precision) are at validation, not volume; U-Precision’s own prospectus shows wafer-bonding revenue under ¥30M (about US$4M) a year, prototype scale. Every publicly torn-down Ascend 910C wears foreign HBM2E (Samsung and SK hynix parts, bought before the ban), and Huawei’s in-house HBM (HiBL) feeds the new 950 series which probably draws from the same CXMT DRAM pool, not the 910C workhorse. Three free evidence lines (tool-vendor filings, the CXMT prospectus, back-end capacity) converge on the same low number for domestic good stacks in 2026.

How to read it: each row is an independent estimate of China’s 2026 domestic supply of good HBM stacks. Dot = central value, bar = stated range, green band = where three of four lines cluster (~1.5–3M). What to see: the ~7M outlier partly measures wafer capacity rather than good stacks, and is weakly supported by the tool and back-end evidence (derivation: Part 6); the memory controls are why the low cluster is the truth. HuaweiFabHunt Stage 49, June 2026.

That is what a control working looks like in the data: a prospectus with a missing product line, a slipped yield curve, a frozen vendor, a teardown full of pre-ban foreign memory. These controls did not slow China down everywhere. They created the single constraint the rest of this series measured.

What leaked, and how

Now the other column, itemized by mechanism: the mechanisms, not the volumes, are the policy lesson.

Leak 1: anticipatory stockpiling. The announcement is a purchase order. The fielded Ascend 910C runs on TSMC silicon. Teardowns date the logic dies to before TSMC’s September 2020 Huawei cutoff, packaged as late as October 2024, topped up at scale through the Sophgo shell channel: roughly 2.9 million Ascend-class dies (about US$500M of wafers) obtained from TSMC before teardowns exposed the channel. Note what that means: essentially every die was fabbed legally as far as TSMC knew when the wafer ran, first inside the 2020 rule’s announced-to-effective window, then through a customer-screening seam uncaught for years. The same mechanism front-ran the memory ban that worked: supplier-side reporting behind the upper-end stockpile estimate has roughly 7 million HBM stacks moving in the one month between the December 2024 rule’s announcement and its effective date, within a total pre-ban import of ~5–13M stacks. Every control in this story was pre-bought against. The die-bank is exhausted (early 2026) and the imported HBM ran out around end-2025. Stockpiling bought China roughly two years of deployment (the 2024–25 wave), not a capability. But the mechanism is structural: a control regime that telegraphs its rules funds its own circumvention window.

Leak 2: the carve-out era. The NVIDIA H20 was not smuggled. It was engineered: a China-spec accelerator designed to sit just under the October 2023 performance thresholds. And it shipped over a million units through 2024 and into 2025, before the April 9, 2025 license requirement closed the channel. For over a year, the single largest inflow of AI compute into China was legal by design. And by 2026 Beijing’s own regulators were probing the H20 for backdoors. I label the carve-out a policy choice, not an enforcement failure; whether it was right depends on objectives outside this dataset. On the grading rule (did the controlled thing arrive at scale?) it delivered more compute than every smuggler combined.

Leak 3: smuggling. Real, bounded, not decisive. The best public estimate (CNAS) puts smuggled advanced NVIDIA chips at a median of ~140k in 2024 (wide band), with at least US$1bn flowing in 2025 and enforcement visibly tightening. Scale it honestly: 140k a year is more than half of China’s entire domestic 2026 ceiling (smuggling matters), but a minority share of the ~700–805k accelerators China actually fielded in 2025, far behind the stockpile and the H20. Smuggling is a tax on the controls, not a hole in them.

Leak 4: the DUV non-control. The deepest leak was mostly legal the whole time. About 90 ArF-immersion scanners (the mid-tier DUV class that SMIC’s 7nm multipatterning actually runs on) shipped in 2024 alone, roughly 70% of ASML’s global immersion output, atop the 400+ DUV tools of 2019–2023; total wafer-fab-equipment imports ran $33–41bn in customs terms in 2024 (SEMI’s consumption figure: $49.6bn). The Dutch restrictions bit only at the top of the immersion range, late. The result is measured in this atlas: logic capacity has 24–60× headroom over what the memory supply can feed (Part 6). China’s logic abundance is not only an engineering achievement. It is partly a policy outcome: the line was drawn at EUV and the highest-end immersion tools, and everything below it shipped in volume.

One number ties the column together. China fielded ~700–805k accelerators in 2025; its domestic ceiling that year was a small fraction of that. The difference is the leakage. And all three big channels are now closed or exhausted, which is why 2026 is the crossover year when shipments fall back onto the domestic ceiling the memory controls built.

The chokepoints that held are not American

Read the worked column again; notice the flags. The bonders that gate HBM stacking: Hanmi, Korea (~90% of HBM3E-grade TCB), with ASMPT and BESI behind it. The HBM incumbents whose parts China stockpiled: Samsung and SK hynix, Korea. The scanners: ASML, Netherlands. Much of the deposition, etch, and test fleet filling the rest of a fab: Tokyo Electron and its Japanese peers. The one meaningfully American chokepoint (NVIDIA’s chips themselves) is precisely the layer that leaked, because chips are small, fungible, and bankable in a way a bonder installed base is not.

So the regime that demonstrably works is, structurally, a coalition artifact. US rules supplied the legal framework: the foreign-direct-product reach, the entity lists, the BIS site licenses. The physical denial happens in Suwon, Veldhoven, and Tokyo. Unilateral US action reaches US-origin technology, US persons, and anything built with US tools (which is a lot), but not the decision, made in an allied capital under its own politics, of whether a Korean bonder vendor keeps shipping. The 2025 customs data shows the seam. US-origin equipment imports fell ~34% while totals held and Singapore and Malaysia posted record transshipment-flavored flows: the rules held; the geography routed.

That makes alliance management, not rule drafting, the load-bearing variable. And there is a live test case as of June 2026. A Korean brokerage note (May 22, 2026; single-source, expectation not shipment, flagged TENTATIVE in my tracker) expects Hanwha Semitech to diversify its bonder supply toward Taiwanese and Chinese customers. If a second Korean bonder maker re-opens what Hanmi closed, the scorecard’s binding control erodes, not because BIS repealed anything, but because the coalition’s weakest commercial incentive found a gap. That is the Hanwha wobble; it sits at the top of the watch list. The verdict, compressed: export-control durability is not a Washington product. It is an alliance product, renewed or not in Seoul, The Hague, and Tokyo every quarter.

What the evidence says about leverage

Analysis, not advocacy: this dataset tells nobody what to want, only what moved.

Where control leverage actually lives. On five years of evidence, leverage concentrates where three properties coincide: the target step young (no installed base to coast on), the supply concentrated (one or two allied vendors), and the dependence continuous (service, spares, recipes, not a one-time purchase). HBM-grade bonders score three for three; that control bent the buildout. Finished chips score zero: many intermediaries, infinitely bankable; that control leaked through every seam it had. Lithography sits between: concentrated and service-dependent, but controlled too late and too high in the range to deny the 7nm-class capacity this story runs on. The transferable lesson: the unglamorous back-end memory step nobody photographs was worth more than the entire chip-level control architecture, at a fraction of the diplomatic cost.

The honest counter-case. The standard argument against all of this: controls accelerate indigenization. Every ban is a subsidy to a domestic toolmaker. The evidence here says true, and bounded. The push is real and visible in my own tracker: domestic bonders at validation, a domestic immersion scanner in trial at SMIC, CXMT sampling HBM3 to Huawei. But Part 8 priced the counter-case: run China’s own demonstrated ramp speed against the memory gap and domestic HBM self-sufficiency lands around 2033, band 2031–2038. That is a projection with a stated band, not a certainty. The controls did not stop indigenization; nothing stops indigenization. On this evidence they bought roughly a decade of binding constraint, paid for in an accelerated and now self-sustaining Chinese tooling program. Whether a decade of constraint is worth a permanently motivated competitor is a values question. The decade itself is a measurement.

The watch: graded in public

A scorecard that only grades the past is punditry. The method this series ran on (falsifiable triggers, stated in advance, checked on a calendar) now applies to its own conclusions. The apparatus, live:

How to read it: each row is one of the seven levers that could move the HBM-bound ceiling; position is readiness-to-fire, from “not started” to “volume (fired),” scored June 2026. What to see: the binding back-end levers (W1 bonders, W3 XMC) sit at validation; CXMT HBM3 (W5) slipped the wrong way; only the merchant cohort (W7) is firing, and it divides the pool rather than growing it. Time-box note: the June 9, 2026 re-check moved W4 (Ascend 950) from 2.0 to 2.5 on mass-production reports (demand-side news, supply unverified). HuaweiFabHunt Stage 44/55b, June 2026.

The five triggers, status as of June 2026 (none has fired):

A domestic HBM-grade bonder qualifies at volume yield. Status: validation. Naura’s hybrid bonder passed customer-side process verification in March 2026; nothing domestic ships HBM stacks at volume with acceptable KGSD yield. The highest-leverage lever on the board, and the one the Hanwha wobble could substitute for from outside.

CXMT reaches HBM3 mass production in 2026 at healthy yield. Status: slipped to late-2026/2027, production yield reported under 50%; samples to Huawei (April–May 2026, CN-sourced, tentative). The slip pins the ceiling at the low end.

Volume HBM from a second source (SwaySure or XMC) before 2027. Status: SwaySure sampling, no volume cleanroom observed as imaged January 2026; XMC pre-volume, its HBM phase imagery-opaque in the February 2026 frame. (Capacity detail: Part 6.)

Confirmed several-hundred-thousand Ascend 950-series shipments on in-house HiBL memory. Status: 950PR reported in mass production since April 2026 with a sold-out order book (demand-side reporting; HiBL volume supply unverified). This is the Q3-2026 check: confirmed volume shipments would force a re-run of the ceiling model.

A teardown surfaces an all-domestic 910C: SMIC die plus Chinese HBM. Status: every public teardown to date shows TSMC-stockpile silicon wearing foreign HBM2E.

Plus the demand-side commitment from the companion project: the stranded-shell forecast (China’s AI data-center buildout producing underfilled shells) gets checked by re-imaging and utilization disclosures within 6–12 months (Part 7 owns that prediction and its receipts).

Together these become the LIMFAC Watch (LIMFAC: the limiting factor, the input that caps output no matter how much else you have): a quarterly issue that re-checks all seven supply-side levers and the data-center forecast, re-runs the model when a trigger demands it, and (the part I care about) grades the previous issues’ predictions in public. One honesty note: the binding HBM step is imagery-opaque at every site, so the watch reads filings, prospectuses, tool-vendor disclosures, and teardowns, not pixels. I just spent a post grading BIS against the ledger. The same standard applies to me. The predictions above are dated, sourced, and falsifiable; subscribe and you will watch them verified or watch them break. Either outcome is the product.

Bottom line

Five years of export controls did not stop China’s AI buildout, and did not fail against it either. They sorted it: chips leaked, tools held, and the tools that held were allied tools. Controls are one of two non-kinetic levers this series mapped; Part 9 walked the other: exposure. Controls are not a wall. They are a clock. And the watch list above is how you read it.

I am going to be able to go to bed before midnight for the first night in too long. Exeunt

Receipts

Control-by-control sourcing on my substack

WORKED: HBM ban (rule dated Dec 2, 2024; effective Dec 31, 2024; controls HBM above a 2 GB/s/mm² memory-bandwidth-density threshold, capturing HBM2E and everything newer) → fielded 910C wears pre-ban foreign HBM2E (teardown-secondary, TechInsights via media); imported stockpile ~5–13M stacks, exhausted ~end-2025 (AC-07, med-high); CXMT STAR prospectus (filed Dec 2025, cleared May 2026) discloses no HBM line (primary filing).

WORKED: HBM-grade bonder halt (Hanmi, ~90% HBM3E TCB share, halted China shipments May 2025; TrendForce 2025-05-13) → domestic bonders validation-stage (Naura process-verification Mar 2026; U-Precision prospectus <¥30M/yr wafer-bonding revenue); W1 not tripped, volume 2027+ (Stage 49 tool-vendor proxy, high confidence).

WORKED: VEU revocation (eff. Dec 31, 2025; 90 FR 42321) + 2026 BIS annual site licenses → foreign-owned fabs in China node-frozen; nationalization adds ~0 AI compute (AC-04/AC-16, high).

LEAKED: anticipatory stockpiling. ~2.9M TSMC Ascend dies via the Sophgo channel (~US$500M of wafers), dies pre-Sept-2020 vintage, packaged Oct 2024, exhausted early 2026 (AC-06, high; Stage 36/49); ~7M HBM stacks reported moved in the Dec-2024 rule’s announcement-to-effective month (within the ~5–13M total; supplier-side reporting).

LEAKED: H20 carve-out. >1M units, ~US$12–15bn, late-2024→April 9, 2025 closure; ~$4.5bn NVIDIA write-off (Stage 36).

LEAKED: smuggling. ~140k/yr advanced NVIDIA (CNAS median, 2024; wide band), ≥US$1bn in 2025, enforcement rising (Stage 36/43).

NON-CONTROL: DUV. ~90 ArF-immersion scanners to China in 2024 (~70% of ASML’s global immersion output) atop >400 DUV 2019–23; WFE imports $33–41bn customs / $49.6bn SEMI-consumption 2024; US-origin −34% to ~$2bn in 2025 while totals held (Stage 15).

The wobble: Hanwha Semitech China-supply expectation; single Korean brokerage note, 2026-05-22, expectation not shipment, flagged TENTATIVE (Stage 55b).

What would change this scorecard (as of June 2026, none has fired): the five numbered triggers above, plus (6) a confirmed allied re-supply channel for HBM-grade bonders (the Hanwha test), and (7) the data-center stranded-shell re-image coming back full (Part 7’s forecast failing would mean chips arrived faster than this model allows).

Document claims are stamped to filing/publication dates; imagery claims to collection dates (SwaySure as imaged 2026-01-25; XMC as imaged 2026-02-22). Figures: Stage 49 reconciliation and Stage 44 indicator charts, HuaweiFabHunt, June 2026. Facility imagery underlying the atlas © Maxar/Vantor, SkyFi, Esri as credited per frame. The ceiling number and its derivation belong to Part 6; the ~2033 clock to Part 8; the demand mirror to Part 7.