AI Great Powers Part 1: Chinese AI Hardware

Not Blocked. Bottlenecked. Huawei’s financials show China is building an indigenous AI-hardware stack, but memory still gates the scale.

This is Part 1 of a two-part filings series. Part 1 is about the hardware stack: Huawei, Ascend, SMIC, domestic equipment, HBM, packaging, and export controls. Part 2 will ask the companion question: whether China’s AI model builders and cloud companies are spending at anything like the scale of the American hyperscalers.

The classic definition of a Great Power is a country able and willing to take on any other country. By that definition, there are two AI Hardware Great Powers: America and China.

That is a resilience claim, not a parity claim. Layer by layer, the United States and its allies are still ahead. In the comparison I would actually use, the US-and-allied stack leads or ties on eight of nine layers: chip design, leading-edge logic, HBM, packaging, EDA, equipment, systems integration, and capital. China scores weakly on the four hardest physical chokepoints: logic, HBM, EDA, and equipment. The one layer where China clearly leads is power, which is useful for brute-force deployment but is not a chip capability. For this piece, “AI Hardware Great Power” means something narrower and more falsifiable: a country with enough design talent, capital, foundry access, memory path, packaging capability, systems integration, power, and political will that the United States and its allies cannot deny it a working AI-hardware stack.

The layer comparison is estimate-grade, not filings proof. Its job is to keep the frame honest: China is not a peer at every layer, but it is too capable and too persistent to be treated as blocked.

I set out to understand the Chinese AI hardware space from financial reporting documentation. Anyone who has run a company has spent a ton of time educating their CFO on the technical aspects of the business. It is a very productive investment because the more the CFO understands the nuance of the business, the more they can squeeze efficiency out of the income and costs.

But financial disclosures are optimized for lenders, auditors, regulators, and investors. They are not optimized for national-security opsec. The audited financial statements and bond prospectuses have to explain the business well enough for outsiders to assess risk, capital allocation, and repayment capacity. That creates leakage.

So I set about mining these for gold dust, and melting them down to make bling.

The project started as a Huawei project.

That was the wrong scope.

Huawei is the flag carrier of China’s indigenous AI hardware effort, but the filings tell you very quickly that Huawei is not the whole story. Huawei hides the most interesting chip-specific economics inside a giant private company. The listed foundry, equipment makers, AI-chip peers, IPO candidates, bond documents, and state-capital vehicles tell the rest of the story.

The answer is annoying in the way useful answers often are.

Huawei’s filings prove the investment is real.

They do not prove the headline chip numbers.

They prove China is building the hardware base.

They also show the near-term gate is not money. It is memory.

The dashboard is the short version: Huawei’s audited numbers show the strategic pivot; the listed supply chain shows the physical buildout; the HBM model shows the near-term gate.

Results Up Front

This is long, and I do not expect most people to read the whole thing. The rest of the post tells you how I got here.

The strategic version is this:

China is not at parity with the United States and its allies in AI hardware. It is behind in leading-edge logic, HBM, EDA, equipment, and power efficiency. But the United States and its allies have not denied China a working AI-hardware stack. They have forced China onto a worse path: more expensive, less efficient, more power-hungry, more state-directed, and more memory-constrained. That is still a real path.

This is the geopolitical mistake to avoid. “Behind” is not the same thing as “blocked.” China can be structurally behind the allied semiconductor stack and still be the second AI Hardware Great Power. A Great Power does not need the best toolchain at every layer. It needs enough domestic capability, money, power, industrial coordination, and political will to keep building after the easy path is cut off. The filings show China doing exactly that.

Huawei is the best visible pressure gauge. Its audited filings show that the sanctions shock turned a large technology company into an industrial-policy platform. R&D rose from CNY 30bn in 2012 to CNY 192bn in 2025, and R&D intensity moved out of the old 14-15% band into the 21-25% range. Depending on the baseline, Huawei spent roughly CNY 250-360bn, or US$35-50bn, more on R&D from 2020 through 2025 than it would have under the old operating model. That is not an Ascend budget. It is the size of the corporate pivot.

The balance sheet shows the other side of the same strategy. Huawei stockpiled components when the supply chain was closing. Raw materials, meaning components and chips, doubled from CNY 35bn in 2018 to CNY 89bn in 2020 while finished goods collapsed. Huawei also has the wallet to keep going: CNY 361-475bn of cash and short-term investments across the relevant period, CNY 1.33tn of assets, CNY 127bn of operating cash flow in 2025, and a bond-disclosed CNY 240.6bn self-funded capital-project pipeline.

The important geopolitical fact is that this is not just Huawei. SMIC, domestic equipment makers, state funds, listed AI-chip peers, and IPO candidates are all part of the same mobilization. SMIC capex moved from roughly US$1.8bn in 2018 to about US$8bn a year. SMIC capacity grew about 2.6x. NAURA and AMEC grew about 10x. Big Fund III is about US$47.5bn. This is not a normal company strategy. It is national substitution under pressure.

The near-term chokepoint is not Huawei’s willingness to spend. It is memory. A transparent HBM model puts the 2026 high-end Ascend production ceiling around 250k-650k accelerators gross, not a few million. Once packaging yield is made explicit, the base deliverable number is lower, about 488k. Even the all-favorable stress-test corner is around 1.2M, still short of the “few million” claim. The decisive swing factor is foreign HBM stockpile exhaustion and domestic HBM yield, not generic wafer capacity.

That ceiling matters, but it does not make the threat imaginary. Unit counts are the wrong final metric. In effective compute, the Ascend 910C is roughly 0.8x an H100 but roughly 5x the H20 that US controls allowed Nvidia to sell into China. Export controls took away an easy import path and forced China onto an inferior domestic path. They taxed capability. They did not erase it.

The policy implication is uncomfortable. Export controls bought time and imposed cost. They did not create a permanent wall. If the United States wants the time to matter, the next game is not just GPU export rules. It is HBM controls, advanced packaging, semiconductor equipment, datacenter power, allied supplier discipline, and staying ahead faster than China can climb the constrained path.

Part 2 of this series is the demand-side check on this claim. Alibaba, Tencent, Baidu, ByteDance, and iFlytek are real AI actors, but the American hyperscalers are spending vastly more capex. That means the right frame is not “China has caught up.” It is also not “China is blocked.” The contest is abundance versus constraint: the United States has the deeper private-sector hyperscaler capital engine; China has the more urgent state-directed substitution machine.

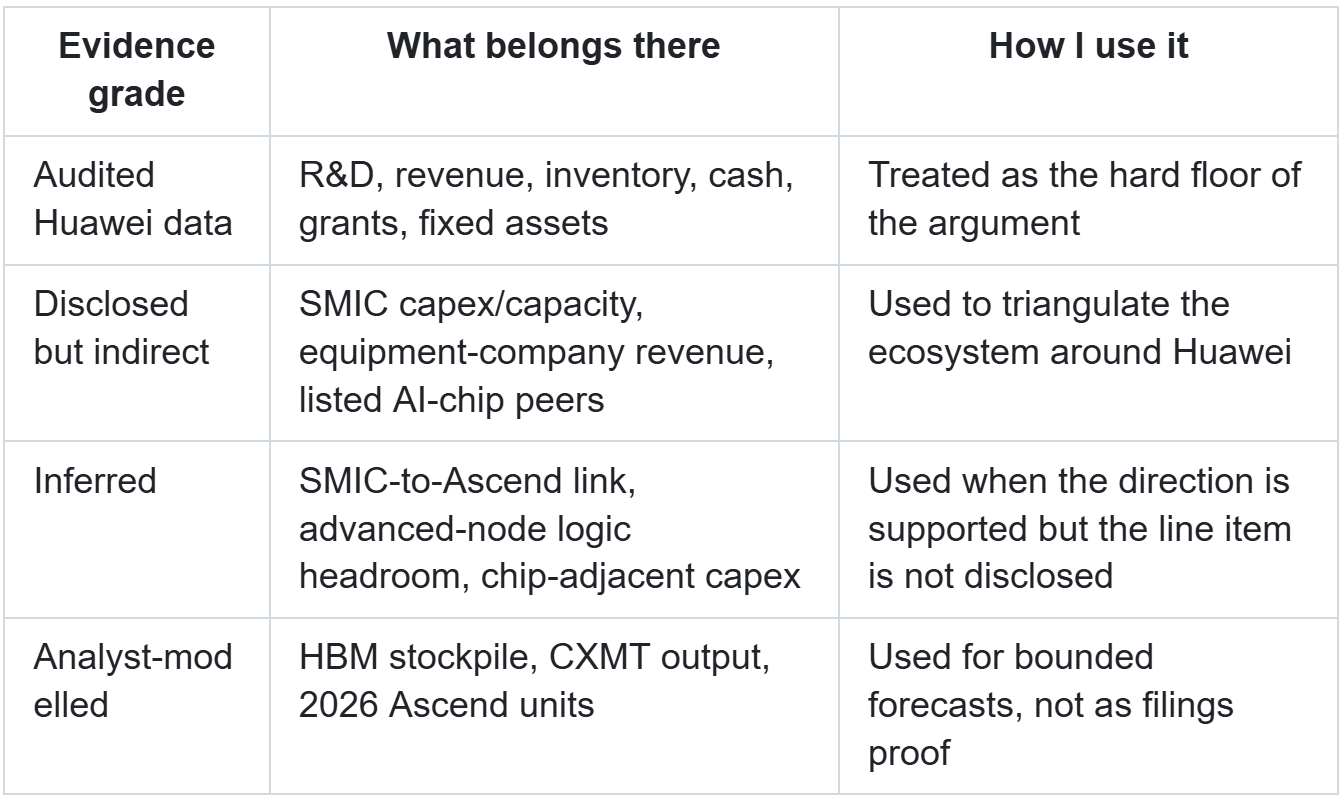

One framing note before the findings: not all evidence in this piece has the same weight.

What I Measured

The project used public financial reporting, not private sourcing.

The first layer was Huawei’s own audited annual reports from 2012 through 2025: revenue, R&D, capex, inventory, segments, fixed assets, cash, staff, margins, and other income.

The second layer was bond and rating-agency documentation. That mattered because bond documents sometimes say the quiet part out loud. Annual reports are written for broad stakeholders. Bond investors want to know what the company is spending money on and whether it can pay them back.

The third layer was the listed supply chain: SMIC for foundry capacity, domestic semiconductor-equipment firms for the tooling ramp, and the state semiconductor funds for capital mobilization.

The fourth layer was listed AI-chip peers. Huawei hides Ascend economics. Cambricon, Hygon, Moore Threads, MetaX, Biren, Iluvatar, and Enflame do not have the same luxury once they list or file to list. Their filings show what chip-specific R&D intensity, losses, inventory, and customer concentration look like when the curtain is not drawn.

The final layer was a claim ledger. I took public claims and asked a simple question: does this map to something in the filings?

Some claims do. Some do not.

That distinction is more important than the individual scorecard.

The Central Problem

Huawei is employee-owned and not stock-listed.

That sentence sounds like trivia. It is the entire analytical problem.

Huawei publishes audited annual reports. It has bond documents. It has rating-agency disclosures. It has enough financial reporting to study. But it does not disclose a HiSilicon segment. It does not disclose Ascend revenue. It does not disclose AI-chip R&D. It does not disclose chip-unit output.

You cannot read “Ascend investment” off a number.

That leaves two ways to do the work.

One is to make stuff up and launder it through confidence.

The other is to triangulate.

I used the second path. Huawei’s group-level financials show the strategic pivot. SMIC and the equipment makers show the physical buildout. Listed AI-chip peers show the chip-specific economics Huawei buries. Public claims get graded against all of the above.

This is important because the Chinese hardware story is not one company. It is a stack.

Huawei designs systems and accelerators. HiSilicon designs chips. SMIC manufactures logic dies. CXMT is the domestic HBM hope. Domestic equipment makers replace the tools sanctions constraint. State funds and local governments push capital into unlisted fabs and suppliers. Listed peers absorb demand when Nvidia parts get curtailed. IPO markets refill the coffers.

The filings do not let you listen in on the room where it happens.

They give you pressure gauges.

Finding 1: The R&D Step Change Is Real

The cleanest signal in the whole project is Huawei’s R&D intensity.

If the sanctions pivot were small, this chart would not break out of the old R&D-intensity band. It does.

From 2012 through 2020, Huawei’s R&D expense mostly lived around 14-15% of revenue. That is already high. Huawei was never a low-R&D company pretending to be a hardware company. It was a technical company spending heavily.

Then the sanctions era changed the slope.

R&D rose to 21-25% of revenue from 2021 onward. In absolute terms, it went from CNY 30bn in 2012 to CNY 192.3bn in 2025. The decade total now exceeds CNY 1.38tn. About 114,000 employees, roughly 54% of Huawei’s workforce, work in R&D.

The important part is not just “Huawei spends a lot on R&D.”

The important part is “Huawei changed how much of every revenue yuan it reinvests into R&D after the sanctions shock.”

I used a deliberately boring counterfactual. What if Huawei had kept R&D intensity near its pre-sanctions level instead of stepping up into the 21-25% band?

The answer is not a single sacred number. If you use the 2012-2020 average, the gap is about CNY 321bn, or about US$46bn. If you use nearby baselines, the band is roughly CNY 250-360bn, or about US$35-50bn. That range is the right way to read the result.

That is not Ascend spend.

It is not a secret chip budget. It is not proof that US$46bn went into Ascend. It is not purely sanctions, either; the whole AI industry spent more in the 2020s. What it is good for is bounding the size of Huawei’s group-level pivot into self-sufficiency: chips, operating systems, EDA substitutes, Kunpeng, Ascend, CANN, Pangu, CloudMatrix, domestic components, and whatever else is bundled into the group.

The reason to frame it this way is simple. Huawei did not tell us the Ascend number. But the group-level pivot is too large to hand-wave away.

If a company adds something like US$35-50bn of above-baseline R&D after being cut off from foreign semiconductors, and then becomes the national champion for domestic AI accelerators, the burden of proof is no longer on the claim that something changed.

The burden is on anyone pretending the change is small.

Finding 2: The Balance Sheet Shows The Stockpile

The 2019 inventory spike is the most visually obvious fingerprint.

Total inventory jumped from CNY 96.5bn in 2018 to CNY 167.4bn in 2019. That is a 73% increase in one year, right after the May 2019 Entity List action and before the 2020 Foreign Direct Product Rule cut HiSilicon off from TSMC.

But the better evidence is inside the inventory composition.

If this were just unsold finished products, finished goods would have carried the surge. They did not. Raw materials did.

Raw materials went from CNY 35bn in 2018 to CNY 89bn in 2020. Finished goods went the other direction, collapsing from CNY 73bn in 2019 to CNY 14bn in 2022.

This matters.

If finished goods had ballooned, the story could have been “Huawei built too many phones and could not sell them.” That would be bad operationally, but not especially revealing about semiconductor sanctions.

That is not what happened.

The durable build was raw materials. Components. Chips. Scarce inputs.

That is exactly what a competent hardware company would do if it saw the supply chain closing around it. You buy what you can buy while you can still buy it, you spend the next few years learning how to live without the imports, and you encode that strategic materials reserve into your corporate DNA.

The filings do not say “we stockpiled materials.”

The balance sheet says it for them. And it says it year after year after year.

Finding 3: Huawei Has The Wallet

There are two separate questions people often blend together.

First: is Huawei spending heavily enough to build indigenous AI hardware?

Second: can Huawei keep doing it?

The answer to the second question is easier.

Yes.

Huawei had CNY 361-475bn in cash and short-term investments across the relevant period, CNY 1.33tn in total assets, CNY 600bn in equity, and CNY 127bn of operating cash flow in 2025.

That does not mean every project succeeds. Money does not solve EUV. Money does not solve HBM yield. Money does not make a 7nm process into a 3nm process.

But money does solve persistence.

The bond and rating documents make that point more strongly than the annual report. They disclose a CNY 240.6bn in-progress capital-project pipeline, with CNY 90.2bn already invested, 100% self-funded. The projects include a Gui’an cloud data center, a Songshan Lake high-end R&D campus, and a Shenzhen pilot/trial-production center.

The bond documents matter because they show named, self-funded projects the annual report leaves blended into the group.

Bond proceeds fund working capital.

The strategic capex is internally funded.

That is why it is invisible as a neat chip line item. It is not a special-purpose public-market financing with a clean investor deck. It is buried in a giant company’s cash-funded capital plan.

This is the CFO version of camouflage.

Not “we have no spend.”

“We have spend so blended into the company that you cannot isolate it.”

Finding 4: State Support Is Visible, But Not At Headline Scale

One of the public claims is that roughly US$30bn, or about CNY 215bn, of state funding went to Huawei-linked fabs.

Huawei’s own filings do show state support.

Government grants recognized in income rose from about CNY 1.5bn before 2019 to a peak of CNY 7.3bn in 2023. Cumulative grants from 2020 through 2025 were about CNY 29bn.

That is real money.

It is also nowhere close to US$30bn.

So the right conclusion is not “state support is fake.”

The right conclusion is “state support to Huawei itself is visible and rose materially, but the big fab money is mostly outside the consolidated Huawei group.”

This is why the ledger grades the claim as partially corroborated. The direction is right. The entity is wrong. The accounting perimeter matters.

I know “accounting perimeter matters” is not the kind of sentence that lights up a room.

It is the sentence that keeps you from being fooled. I couldn’t find the rumored big state subsidized fab in any corporate filings.

Finding 5: The Buildout Is National, Not Just Huawei

Huawei’s filings are not enough because Huawei does not run the whole hardware stack.

The supply-chain filings fill in the shape.

Huawei’s R&D rises, but SMIC and the equipment makers rise faster. That is the fingerprint of a national stack, not a single-company capex story.

SMIC capex went from roughly US$1.8bn in 2018 to about US$8bn a year by 2025. SMIC year-end capacity grew from about 406k to about 1.06M 8-inch-equivalent wafers per month, and 2026Q1 reached about 1.078M. Revenue set records. Utilization stayed high.

SMIC never says “we are making Huawei Ascend dies.”

It does not have to say it for the capex ramp to matter. The public link from SMIC to Ascend is sourced assessment. The capacity, capex, and revenue are disclosed facts.

Domestic equipment companies tell the same story. NAURA and AMEC grew about 10x since 2019. The state Big Fund Phase III is about US$47.5bn and targets equipment, HBM, and AI chips.

This is why a Huawei-only frame is too narrow.

If you only read Huawei, you see a private company that spends more on R&D after sanctions.

If you read the stack, you see foundry capacity, domestic tooling, state capital, cloud demand, chip startups, and listed peers all moving in the same direction.

That does not prove every public claim.

It proves the mobilization is real.

Finding 6: Listed Peers Show The Economics Huawei Hides

Huawei does not disclose Ascend economics.

China’s listed AI-chip firms do.

That is the disclosure window Huawei denies us.

Cambricon is the cleanest pure-play comparator. For years, its R&D intensity ran 122-209% of revenue. In FY2022 it was around 209%. This is what “investing heavily in indigenous AI chips” looks like when the chip line is visible.

Then 2025 happened.

Cambricon is the cleanest public test case for what happens when curtailed Nvidia demand gets pushed toward domestic accelerators.

Cambricon revenue rose 453% to CNY 6.5bn and the company posted its first annual profit, CNY 2.06bn, after eight straight years of losses.

That is not a small demand-side signal.

That is the export-control substitution effect showing up in audited numbers.

Cambricon also stockpiled like Huawei. Inventory rose 179% to CNY 4.9bn, about 37% of total assets, with wafer pipeline and supplier prepayments used to lock scarce domestic foundry capacity.

The point is not that Cambricon equals Huawei. The point is that chip-only R&D intensity is far higher than Huawei’s blended group average.

This is why Huawei’s 22% group-level R&D intensity is both huge and misleading.

It is huge because Huawei is enormous.

It is misleading because chip-only companies often have to spend 100-600% of revenue on R&D while they are building the product and market. Huawei’s group average masks the Ascend economics.

Hygon is the profitable AI-compute heavyweight. It grew revenue from CNY 2.3bn in FY2021 to CNY 14.4bn in FY2025, with R&D up to CNY 4.6bn.

Then there is the IPO wave.

The IPO cohort makes the same point another way: when indigenous GPU companies disclose their books, the R&D intensity looks extreme.

Moore Threads, MetaX, Biren, Iluvatar, and Enflame raised more than US$3.5bn in roughly 10 weeks across the 2025-2026 listing wave. Their filings show extreme chip-specific R&D. The five GPU startups spent CNY 5.2bn on R&D against CNY 2.8bn of revenue in FY2024.

Again, these are not Huawei.

That caveat matters.

The assessment is not “Ascend revenue equals Cambricon revenue” or “Huawei has Cambricon’s margins.” The assessment is narrower: listed chip firms show the economic pattern Huawei hides, which is years of heavy chip-specific R&D, stockpiling, and demand substitution after controls.

They are smaller. They are product-distinct. Their customer bases and accounting quirks differ. Their R&D-to-revenue ratios also look extreme partly because the revenue denominators are small. So I am not using them as numeric proxies for Ascend. I am using them as visible examples of the pattern. They show what Chinese indigenous AI-chip programs look like when the chip business is visible. Whether Ascend’s own economics match any of them is exactly the thing Huawei’s filings will not tell us.

The peer filings confirm two things:

First, indigenous AI-chip investment is real and large.

Second, the controls shifted demand into domestic silicon rather than stopping demand from existing.

Finding 7: Logic Dies Are Not The Gate

The instinctive bottleneck story is “SMIC cannot make enough 7nm logic dies.”

That story looks wrong.

The chart is the bottleneck argument in one picture: logic capacity has headroom; HBM does not.

The bottoms-up reconciliation uses a 665 mm2 Ascend-class die and about 76 dies per wafer. The less certain input is SMIC’s 7nm-class capacity. Published estimates do not agree. Some put the relevant line around 20k wafers per month. Others put the 2025-2026 range closer to 45-60k. Yield is also uncertain, somewhere around 30-55% in the useful range.

That sounds messy because it is messy. But the conclusion does not require false precision. At the realistic HBM ceiling, the wafer demand is small against every plausible logic-capacity case. On the higher capacity estimates, 650k high-end accelerators use only a few percent of the line. Even on the lower 20k-wafer estimate, they are still not enough to make logic the gate. In the stacked pessimistic case, with low capacity, low yield, smaller die count, and Ascend getting less than a third of the line, the logic side still builds several times more 910C-class packages than the available HBM can populate.

SMIC’s disclosed largest customer was 8.1% of 2024 revenue. That does not prove a Huawei link. It does show that a meaningful Ascend allocation can fit inside SMIC’s customer-concentration disclosure because advanced-node wafers are a thin slice of SMIC’s total mature-node-heavy business.

Logic capacity is not irrelevant. Yield matters. Node maturity matters. EUV absence matters. But I am not claiming a precise headroom multiple. I am claiming the durable thing: in 2026, the binding number is HBM stacks, not logic wafers.

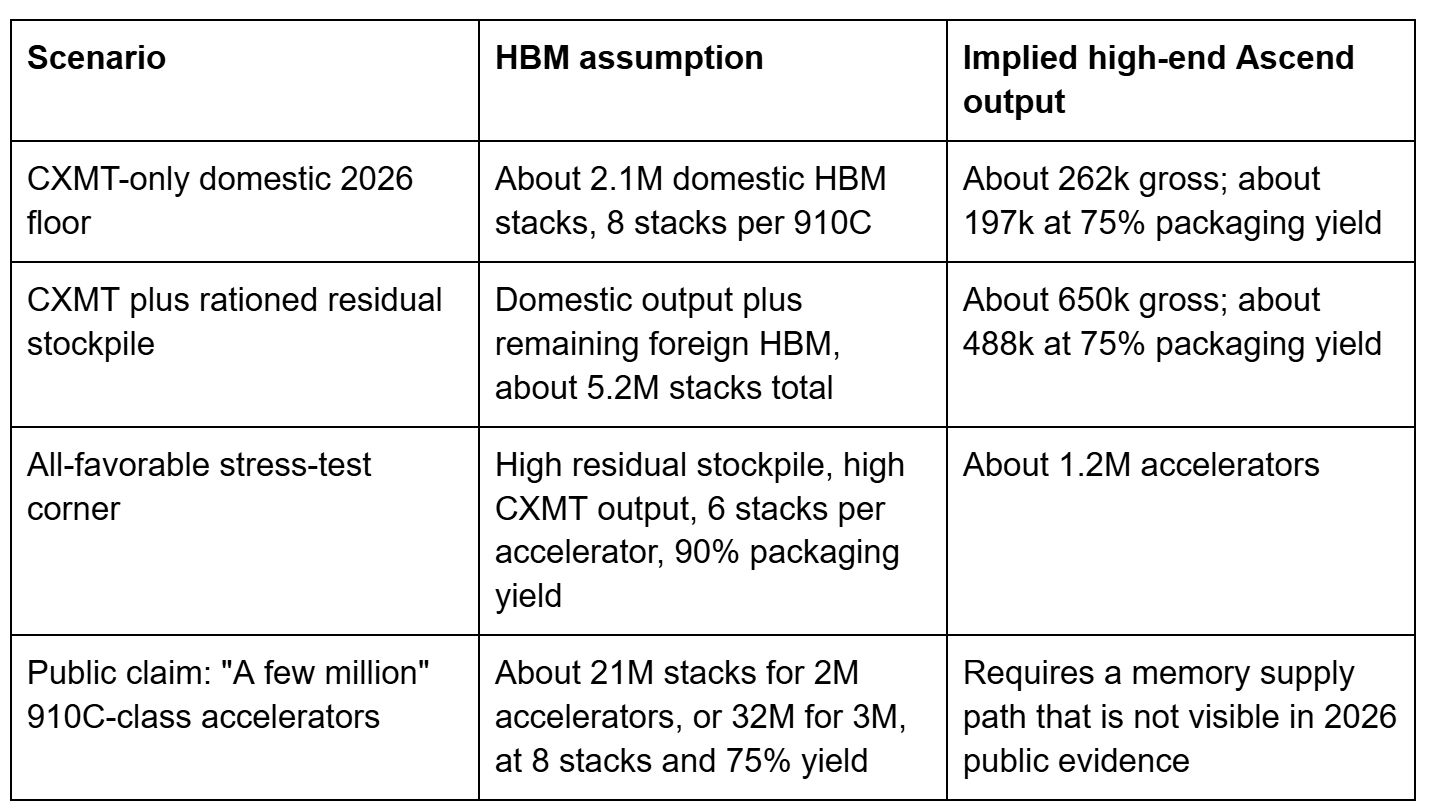

The gate is HBM.

High-bandwidth memory is not just another component. For an AI accelerator, it is the thing that lets compute be useful. The 910C uses 8 HBM stacks. The buildable accelerator count is basically:

available HBM stacks / stacks per chip

Before packaging yield, that is the model. With packaging yield, the number only moves down.

The “few million” debate is easier to understand backwards. To build 1M high-end accelerators at 8 HBM stacks each and 75% packaging yield takes about 10.7M HBM stacks. To build 2M takes about 21.3M. To build 3M takes about 32M. The plausible 2026 supply pool in the base model is about 5.2M stacks.

The model is intentionally simple. It is also not a filing-derived fact. The foreign stockpile depth, CXMT’s 2026 output, and the 8-stack 910C assumption are heavily downstream of the same analyst work, especially SemiAnalysis. I am re-running and stress-testing those inputs, not discovering them from Huawei’s books. Treat 250k-650k as a bounded guess, not a filing fact.

That caveat cuts both ways. If the HBM stack count is wrong, the output estimate moves. But the stress test says which input matters. The swing factor is not whether CXMT makes 2.0M or 2.25M stacks in 2026. The swing factor is how long the foreign HBM stockpile lasts, whether Huawei can use fewer stacks per high-end part, and whether packaging yield is materially better than expected.

The HBM model puts the 2026 CXMT-only domestic floor around 262k high-end Ascend accelerators gross, with a range of about 250k-281k. If Huawei can ration residual foreign HBM stockpile into 2026, the gross ceiling rises toward about 650k, with wider uncertainty. With a 75% packaging-yield assumption, that 650k gross case becomes about 488k deliverable accelerators.

That is meaningfully below “a few million.”

The decisive swing factor is when the foreign HBM stockpile runs out. The secondary swing factors are CXMT HBM3 qualification, die-to-stack backend yield, packaging yield, and whether Huawei’s in-house memory efforts scale faster than expected.

This is the place I would watch.

Not because logic does not matter.

Because the logic-side capacity has headroom and the memory-side capacity does not.

Finding 8: Export Controls Taxed China. They Did Not Wall It Off.

The original policy premise was that export controls would set back China’s AI program.

That is partly true.

The narrower Huawei premise is definitely true. Huawei revenue fell 29% from CNY 891bn in 2020 to CNY 637bn in 2021. The consumer business was hammered. Net margins were crushed in 2022. The company then recovered to CNY 881bn by 2025, with ICT Infrastructure as its largest segment and Cloud, Digital Power, and Automotive becoming more important.

So yes, Huawei was set back.

The broader AI-program claim is more subtle.

In effective compute terms, the Ascend 910C is roughly 0.8x an H100 on BF16 compute but roughly 5x the H20 that controls allowed Nvidia to sell into China. CloudMatrix brute-forces scale: it can beat Nvidia’s GB200 NVL72 on raw compute, but at much worse power efficiency.

This is why units are the wrong final metric. The same unit count can mean very different capability depending on which chip you compare against.

The right framing is not “controls failed” or “controls succeeded.”

The right framing is “controls imposed a tax.”

They forced China onto a more expensive, less efficient, supply-constrained path. They made HBM a bottleneck. They forced domestic substitution. They likely slowed and distorted the buildout.

But they did not deny capability.

If the 2026 ceiling adds about 200k-500k H100-equivalents per year, that is roughly comparable to the H20 fleet the controls removed. It is less efficient, harder to scale, and constrained by memory. It is still real compute.

This is the uncomfortable policy answer.

The controls bought time and imposed cost.

They did not create a permanent wall.

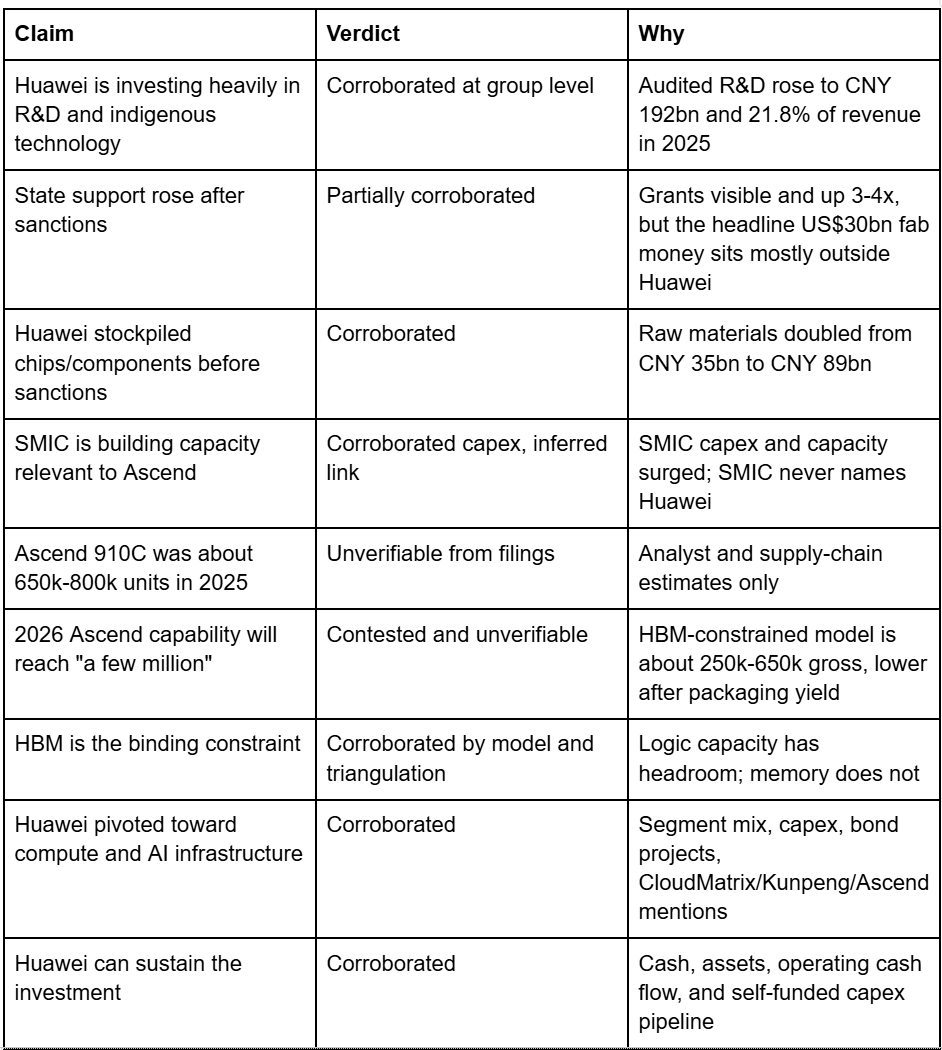

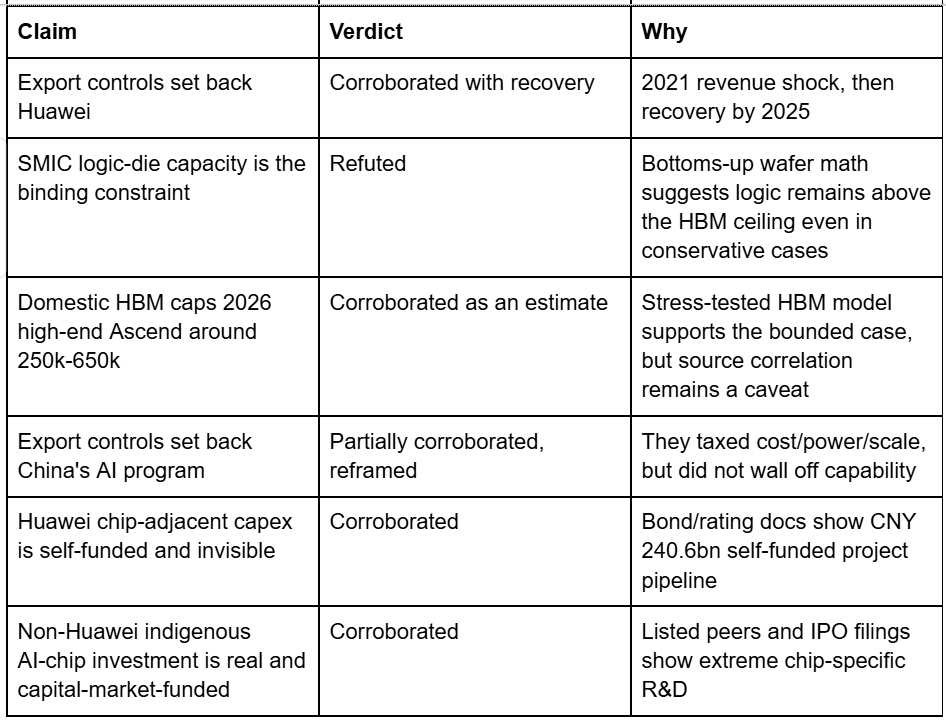

The Claim Ledger

Here is the condensed version of the claim ledger.

The pattern is the whole point.

The blog-facing provenance file turns the ledger into a source trail. Across the 15 condensed claims, the current status is 10 corroborated, 2 partially corroborated, 1 refuted, and 2 contested or unverifiable. That count is less important than the sorting: the claims grounded in audited financials are much stronger than the claims grounded in chip-unit forecasts.

Claims tied to total R&D, inventory, capex, cash, grants, or listed-peer filings usually hold up.

Claims tied to exact Ascend units, secret fab dollars, or near-term millions of chips do not come from Huawei’s filings.

They may be true. They may be false. The filings cannot verify them.

That is not a limitation to bury in the methodology.

That is one of the main findings.

The Best Arguments Against This

The strongest counterargument is still HBM. Huawei may have more memory progress than the public record shows. The new in-house-HBM evidence does not prove that yet. HiBL and HiZQ are real Huawei roadmap items, but they are proprietary memory standards for the 950-series, not disclosed finished-stack volume for the 910C. CXMT has shipped HBM3-class samples to Huawei, but the public evidence still looks like sampling and qualification, not 2026 volume. If that changes, the ceiling changes quickly.

The second counterargument is that the SMIC advanced-node capacity estimate may be wrong. That is fair. The published 7nm-class estimates disagree widely. The reason I still do not think logic is the 2026 gate is that the conservative wafer math leaves several times more logic capacity than the HBM supply can populate.

The third counterargument is that the unit discussion may be too focused on 910C-class high-end accelerators. China could choose a broader mix of lower-end accelerators, domestic memory configurations, and rack-scale systems that create useful AI capacity without matching the high-end 910C envelope.

The fourth counterargument is that the filings are too aggregated to support any strong chip-specific conclusion. I agree with the narrow version of that critique. The filings do not measure Ascend spend or output. The stronger claim I am making is that the filings prove the group-level redirection, and the supply chain bounds the likely physical constraint.

Those are the right places to attack the conclusion. Not “Huawei’s R&D is fake.” Not “China has no AI hardware capability.” The real fight is memory volume, packaging yield, advanced-node allocation, and system-level efficiency.

What Would Change My Mind

There are a few things that would move the conclusion.

First, a real HiSilicon or Ascend segment disclosure. I do not expect this. But if Huawei ever discloses chip revenue, chip R&D, chip gross margin, or unit output, that would replace a lot of assessment.

Second, credible evidence that CXMT HBM3 backend yield is materially better than the current base case. This is the biggest upside break in the 2026-2027 forecast.

Third, evidence that Huawei’s in-house HBM efforts are shipping in volume, not just sampling or appearing on a roadmap. A named fabricator, finished-stack output, customer qualification, or an independent teardown would matter. A press claim that HiBL or HiZQ exists is not enough.

Fourth, node-specific SMIC capacity disclosure. SMIC gives capacity and capex, but not the exact advanced-node mix. The logic-headroom conclusion is robust to a range, but real node disclosure would tighten it.

Fifth, a public reconciliation of Ascend shipments to HBM procurement. If someone can credibly show HBM stacks in and accelerators out, the unit debate gets much cleaner.

Sixth, a meaningful policy change reopening HBM supply. Yeah, I’m laughing out loud too as I type that.

What To Watch

If you are tracking this as an operator, investor, or policy person, I would watch five leading indicators.

First, foreign HBM stockpile exhaustion. That is the single biggest 2026 swing factor, and also the hardest to verify from public evidence.

Second, CXMT HBM3 qualification and yield. Press releases do not matter much. Finished, yield-good stacks do.

Third, Samsung and SK Hynix China-HBM licensing rules. The tap reopening would change the model quickly.

Fourth, Huawei rack-scale systems. CloudMatrix-style systems show how China is compensating for weaker chips: more power, more packaging complexity, more systems engineering.

Fifth, listed-peer inventory and prepayments. Cambricon-style stockpiling is the visible tell that companies are locking scarce domestic capacity ahead of demand.

For U.S. policy, that means the next game is not just GPU export rules. It is HBM controls, advanced packaging, datacenter power, equipment substitution, and how fast allied suppliers can stay ahead while China climbs the stack.

The worst way to follow this story is to argue abstractly about whether China is “behind.”

Behind what?

On lithography, yes.

On HBM, yes.

On ability to build useful AI compute at national scale, no.

On power efficiency, yes.

On willingness to spend through the pain, no.

That is why the Great Power framing matters. A Great Power does not need to be the most efficient actor. It needs to be able and willing to keep taking the punch and keep building.

China is doing that.

Methodology And Uncertainty

The extraction pipeline used public PDFs, annual reports, bond and rating documents, public financial tables, listed-company filings, and reproducible scripts in the research repository.

For Huawei’s own annual-report metrics, extracted values were validated against an independent Huawei bond-investor-relations table without any detected errors. Computed R&D intensity reproduces Huawei’s stated percentages.

For supply-chain and HBM estimates, the confidence is lower because SMIC does not disclose Huawei-specific revenue, advanced-node capacity, or Ascend shipments; CXMT is unlisted; HBM stockpile estimates are heavily analyst-modelled and partly correlated; and packaging yield is not public.

That is why I keep separating filings from assessment.

The most important uncertainty is not whether Huawei is investing heavily. That is settled at group level.

The most important uncertainty is near-term throughput: how many competitive AI accelerators can be packaged with available, yield-good HBM.

The second most important uncertainty is how quickly China’s memory stack improves.

The third is how much worse power efficiency matters in practice. If Chinese customers have enough power, enough datacenter capacity, and enough political direction, worse perf/W is a tax. If power or cooling becomes binding, it becomes a wall in specific deployments.

Bottom Line

Huawei’s filings show a heavy, audited, sanctions-driven redirection of investment toward self-sufficiency.

They show the R&D step change.

They show the component stockpile.

They show the cash.

They show some state support.

They show self-funded capital projects.

They do not show Ascend as a clean line item.

The supply chain and listed peers fill in the rest of the picture. SMIC and the equipment makers show the physical buildout. Cambricon, Hygon, and the IPO cohort show the indigenous AI-chip pattern Huawei hides. The HBM model shows why memory and packaging, not Huawei’s wallet, gate the 2026 ceiling.

So the honest conclusion is a confident qualitative yes and a constrained quantitative no.

Yes, China is an AI Hardware Great Power.

Yes, Huawei is investing heavily and building real capability.

No, Huawei’s public filings cannot validate the most dramatic chip-specific claims.

No, the 2026 ceiling does not look like a few million high-end Ascend accelerators unless the HBM story changes.

The trajectory is up and to the right.

The constraint is memory.

Part 2 asks the mirror-image question: if China can keep building constrained domestic hardware, are its model builders and cloud companies investing at American hyperscaler scale?

The strategic mistake would be treating “less efficient and supply-constrained” as the same thing as “not capable.”

It is capable.

It is taxed.

That is not the same thing.